A controversial part of Obamacare imposes an excise tax on high cost health plans. Beginning in 2018, the so-called Cadillac Tax will impose a penalty of 40 percent of all costs in excess of $10,200 for employee-only coverage and $27,500 for family coverage. The threshold increases annually with inflation; that is regular inflation, not medical care inflation which rises at more than double the rate of general inflation.

Employers have a few options to avoid the tax. But all are things workers dislike, such as increasing cost-sharing, eliminating covered services, eliminating tax-free dollars for HSAs, HRAs and FSAs and adopting narrow networks.

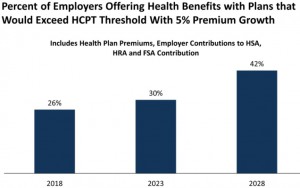

The Kaiser Family Foundation looked at the proportion of firms offering health benefits plans that are expected to reach the threshold.

If you only look at large firms employing 200 workers or more, nearly half (46%) will have health plans subject to the tax in 2018. More than two-thirds (68%) will have health plans subject to the tax by 2028.

The tax exclusion for employee health insurance is worth approximately 40% to 45% (25% marginal tax rate, 15.3% payroll tax and maybe 5% state and local tax). What the Cadillac Tax does is impose a 40% tax on the excess costs over the threshold. What that basically means is the open-ended tax exclusion for employer sponsored health plans has been limited to $10,200 per individual and $27,500 per family.

Pro: Limiting the tax exclusion may encourage health plans to look for ways to reduce medical spending.

Con: Over time more and more people will be subject to the tax.

Should the Cadillac Tax be repealed? Let me know what you think!