Weak Idea at Bernie’s: Bureaucrats Should Not Negotiate Seniors’ Drug Prices

Senator Bernie Sanders and Representative Elijah Cummings — along with a few other liberal Members of Congress — want to change the way Medicare purchases drugs for seniors. It is a popular talking point mainly because many Americans naively assume Medicare does not bargain over the price of drugs. Even President Trump has perpetuated the bogus idea that having the government negotiate the price of drugs would lower Medicare’s drug costs. This may sound appealing to many because drug makers don’t elicit much sympathy these days. Yet, seniors, drugmakers and taxpayers alike have a stake in the outcome because drug therapy is the most convenient and efficient way to care for patients.

Senator Bernie Sanders and Representative Elijah Cummings — along with a few other liberal Members of Congress — want to change the way Medicare purchases drugs for seniors. It is a popular talking point mainly because many Americans naively assume Medicare does not bargain over the price of drugs. Even President Trump has perpetuated the bogus idea that having the government negotiate the price of drugs would lower Medicare’s drug costs. This may sound appealing to many because drug makers don’t elicit much sympathy these days. Yet, seniors, drugmakers and taxpayers alike have a stake in the outcome because drug therapy is the most convenient and efficient way to care for patients.

Medicare Drug Plans. The Medicare Part D drug program is run by private firms, who manage drug benefits for seniors. Medicare drug plans use a variety of techniques to control drug costs, including preferred-drug lists, tiered formularies, use of mail-order drug suppliers, negotiated prices with drug companies and drug distributors, and contracting with exclusive preferred pharmacy network providers. Private drug plan managers negotiate drug prices, often pitting each drug in a given class against competing drugs for a spot in a formulary. A formulary is the schedule of drugs covered by each plan. It varies slightly from one drug to the next, but on average, plan managers obtain discounts of about one-third off list prices. How do they do it? The pharmacy benefit managers (PBMs) who manage Part D drug plans have massive buying power. More importantly they have the ability to say “no” and refuse to cover a given drug if the price is not competitive with what competing drugmakers charge for similar drugs. It’s free market competition. Often times, the winning bidder is guaranteed 85 percent of plan members’ drug business when winning bidders’ drugs are approved for the formulary.

Could Government Get a Better Deal? It’s doubtful. Granted, buying power is important. However, the primary leverage a buyer has is the ability to walk away from a deal and deny a firm its business. The government lacks the willpower to say no in the face of angry seniors convinced they need a drug they heard about on TV. The Centers for Medicare and Medicaid Services (CMS) is run by political appointees. These agencies are overseen by Congress and Congressional committees. Members of Congress often get campaign contributions from the industries they oversee. As you can imagine, if CMS refused to cover a particular drug, Members of Congress from the district where the drug is made may intercede on the manufacture’s behalf. In a nutshell, Congress lacks the political will to effectively negotiate lower drug prices. When CMS inevitably failed to drive prices lower, there would then be calls for outright price controls, with prices dictated by fiat. Most economists agree price controls would result in fewer new drugs coming to market and fewer generic drugs to follow.

History of Success. More than 40 million seniors rely on Medicare Part D for prescription drug coverage. By virtually all measures, Medicare Part D has been a great success. Seniors’ satisfaction rates average about 90 percent. Seniors participating in Medicare Part D pay about one-fourth of the cost of their drug plan, while the government subsidizes about three-fourths of the cost. Though subsidized by Medicare, the premiums seniors pay are a function of the plan they choose — and ultimately of total program expenditures. On average, seniors choose plans with monthly premiums of about $42 for a stand-alone plan.

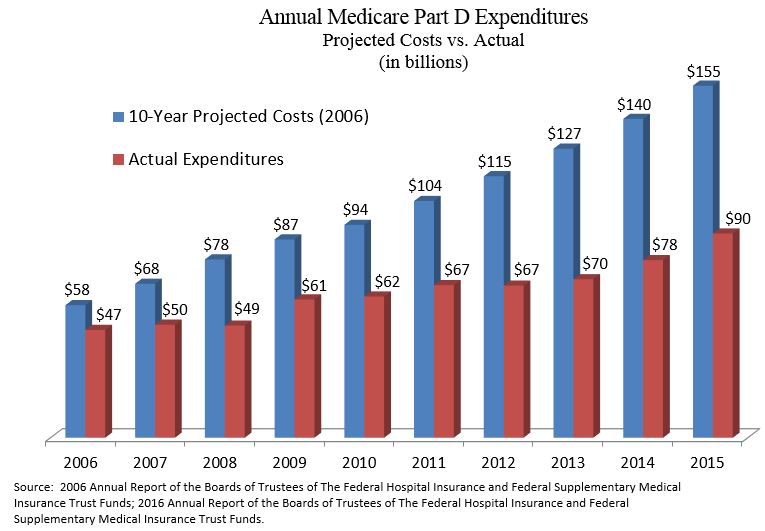

Premiums have remained affordable because drug spending per member has been far lower than projected. Back in 2006, the Social Security and Medicare Trustees projected the program would cost about $155 billion by 2015. Yet the cost in 2015 was only about $90 billion. [See the Figure] Medicare Part D has come in under budget and held seniors’ drug plan premiums in check for one primary reason: vigorous competition among numerous competing plans. Seniors select the plan that best meets their needs, so plan sponsors are constantly looking for ways to earn their patronage. Flexibility of plan design is another reason for Medicare Part D’s popularity. Medicare drugs plans are designed to appeal not just to seniors with high drug costs, but also those who spend little but want affordable protection against unanticipated drug bills.

Bad Solution to a Problem that Doesn’t Exist. Since its inception, the Medicare Modernization Act that created Medicare Part D has included an anti-interference clause. The Medicare program cannot take sides in negotiations among marketplace participants. Contract negotiations between drug makers, pharmacy networks and drug plan sponsors are left strictly to the respective parties.

In this case the status quo is the best possible solution. When politicians talk about the government negotiating Medicare drug prices, keep in mind unelected bureaucrats and political appointees will be the ones negotiating. They will have little reason to drive hard bargains when their Congressional overlords want to protect valuable constituents, who fill their campaign coffers. Without the knowledge that a “losing bid” risks losing out on virtually all business from seniors enrolled in a given Medicare drug plan, drugmakers would have little reason to offer their lowest prices during contract negotiations.

Rx in Medicare is the price we paid for the tax-free HSA for all Americans under the age of 65-years-old. Now we have poor young people paying sky-high payroll taxes so multi-millionaires, like my brother, can set on their boats here in Tampa Bay and scarf down FREE drugs in Medicare.

No wonder young people quit having children, the future taxpayers.

PLUS, Medicare discriminates against Black males, it’s racist.

Bureaucrats Should Not Negotiate Seniors’ Drug Prices and neither should Part D

Devon, I take issue with your positive comments about Part D. Think liquidity constraint and then think how Part is partially responsible for inflationary drug pricing.

“Medicare Part D drug program is run by private firms” … That doesn’t make Part D a free market device. In fact if one wants to give part D a political label they could just as easily label it as fascist.

“plan managers obtain discounts of about one-third off list prices. How do they do it?”

Ever hear of the chargemaster for hospitals? Take a lesson from the chargemaster. I wonder why my Part D insurer pays more for certain drugs than I would have had to pay. I still use my insurer because I only have to pay a fraction of the higher cost price. Recognize that we are paying more than necessary because the taxpayer is blindly subsidizing 75% of the bill. This program is grossly flawed even though “Seniors’ satisfaction rates average about 90 percent.” You could double the price for my car and I would still be satisfied if the I only had to pay for 1/4 of the cost.

“Premiums have remained affordable because drug spending per member has been far lower than projected.”

Of course that happens when 75% of the bill is picked up by the taxpayer and when the insurer doesn’t cover the most expensive drugs. Then the insured either takes a less expensive drug that might not meet patient needs or the patient pays for the drug himself relieving the insurer of that cost!

Let me give you an example, Lunesta, whose list price is somewhere in the range of $300. Check out the Medicare plans and see if any carry Lunesta. How much the insurers have to pay, I don’t know, but it is surely higher than $22 from membership warehouse or healthWarehouse at $54 or $39 from Walgreens in my area based upon some sort of discount. The insurance alternative might be Ambien and they might pay quite a high price for it. But if the patient chooses the alternate drug and pays cash the insurer saves money or if the patient chooses the less expensive medication through the insurer even though it might not work as well the insurer still saves money. They win no matter which choice is made and you will have your opportunity to compare the present costs with the projections and applaud. Multiply this by a whole bunch of similar episodes and there will be lots of savings from prior projections, but quite a loss based upon reality.

We have all been hoodwinked.

I agree with Devon that the current Part D program is working reasonably well, at least for the most part. I also think there is plenty of room to speed up the FDA approval process especially for manufacturers of generic drugs who want to enter the market as new competitors. Hopefully, new FDA Commissioner, Scott Gottlieb, will lead the way to do just that.

One issue that does need attention is to find a way to pass the rebate that payers receive to the insured member who has a high deductible drug or health insurance plan and is exposed to paying the full cost of the drug even when the payer receives a rebate that can easily equal half of its cost. This was most clearly illustrated by the recent furor over the pricing of the Epi-Pen manufactured by Mylan Pharmaceuticals.

I think when liberals talk about Medicare negotiating drug prices, what they really mean is to have Medicare DICTATE drug prices just like they do with services, tests and procedures paid for by Medicare Parts A and B. That way, Medicare won’t have to make coverage or formulary placement decisions. It’s a bad idea pure and simple.

In the pure free market world favored by Allan, most people would not be able to afford to buy the more expensive drugs, especially the specialty drugs which would probably mean that most of them would never have been developed in the first place because drug companies wouldn’t be able to make enough money to cover their costs. This is especially true for specialty drugs aimed at relatively small populations covered under the Orphan Drug Act of 1984 which defines a small population as fewer than 200,000 patients in the U.S.

Finally, most people don’t realize that many of the expensive drugs that need to be infused in a doctor’s office, infusion center or hospital are not included in the cost of the Part D program because they are covered under Medicare Part B.

“Part D program is working reasonably well”

Of course you would feel that way, Barry, since it is a government program and the senior only pays 25% of the actual cost that is grossly inflated. I am going to buy a car tomorrow. I’ve had my eye on a Porsche for $100,000. I’m hoping you and Devon can get the taxpayer to pay for part of it so it only costs me $25,000. I’d give that exchange high marks and a 5 star satisfaction rating.

“In the pure free market world favored by Allan, most people would not be able to afford to buy the more expensive drugs”

You are right. Prevent liquidity constraint from doing its job and thereby let pharmaceutical prices double and triple. Fantastic idea until the prices get so high that even the 10 cent medication increases to unaffordable levels. We have seen that before with the ACA that you have embraced over and over again. You should write a book. “My love affair with socialism”.

Of course one could provide insurance for certain needs instead of insurance to pay for all medications that have been priced based upon the assumption of insurance.

You probably believed Hillary Clinton when Bill was President and Hillary pointed to a poor woman (I think it was all made up) who spent $10,000 on her medications. Hillary gave the diseases and I calculated that using very successful medications I could probably treat the woman for about $300. (The Orphan Drug Act you mention defines an alternative way of producing and paying for certain drugs having high costs. It’s an alternative to the stupidity of Part D.)

Anyway, Barry, Merck tells me your check is in the mail and thanks you for your support in helping them create a higher floor for their drugs while leaving the ceiling wide open.

Ya what Allan said 👍👍

Both Allan and Barry have some good points.

Barry, I have been interested in this proposition of yours

“….the specialty drugs which would probably mean that most of them would never have been developed in the first place because drug companies wouldn’t be able to cover their costs…”

When a drug has a large market like Sovaldi for hepatitis, is this really true?

Even if Sovaldi cost $1 billion to develop, there are at least 2 million potential customers just in the US. At a price of $84,000 a year, and assuming a low cost of production, the maker of Sovaldi would cover their development costs after 20,000 or so patients!!

(I know my numbers are rough)

Bob, you are looking in the wrong direction. Don’t look at the costs and profits of success, that is unwise. How do you compensate those that spent a billion dollars and end up losing money?

I have said this a million times, we pay for capital risk along with costs and time. Creating a new drug or drug class has a high capital risk with many failures along with taking a long time before seeing profits. Those that invest their capital do so to earn a profit and they don’t necessarily care what that investment goes into. Most importantly they invest based upon profit and risk whether it be pharmaceuticals or toys. They might expect a higher return in pharmaceuticals because there might be more losses and a greater time period involved.

In any event these marketplaces for capital act to stablize the markets. If the costs of products are too expensive few if any will invest in those products and the investors will choose to invest in products that are more affordable. If the government artificially lowers profits the investors will flee from that sector.

Bob, have you ever invested in the stock market, real estate etc. yourself where you had to evaluate risks and returns not relying upon a balanced portfolio and other people? If you did, which I doubt, you would be thinking differently.

Allen, I like your point about liquidity constraints.

It reminds me of the debates about college tuition and how it has grown, the more we subsidize it.

In a world without drug insurance, would pharma companies not even develop specialty drugs, some of which are really quite wonderful? (I speak from personal experience.)

Or, would they develop something close to the current drugs but just charge what people could afford without insurance?

In other words, if every country paid for drugs what India or Egypt paid, would advanced drugs disappear?

Personally I doubt it but my knowledge is limited.

“It reminds me of the debates about college tuition and how it has grown, the more we subsidize it.”

You got it.

If liquidity constraint more strongly existed in the pharmaceutical industry likely we would see a few less similar super expensive drugs appearing at the same time. We also might see the scientists looking for ways to make care less expensive which would be a big benefit. Additionally we might see the FDA radically change their rules to promote more innovation and lower the costs of production.

Right now government fashions the removal of money from your pocket in the least recognizeable way possible. That means under many or most circumstances a lot of money is wasted in the process of disguising the theft. Think of the ACA. Why charge the young more? It was a way to obtain revenue without obvious taxation. Why was the penalty not a tax? Because they wanted to hide the tax. AS soon as you recognize that good government is less government, the sooner you will see your aims achieved.

The question about whether to insure the most expensive drugs is a tough one.

If you do insure the drugs, some extra lives are saved. (even if they are only saved for a period of months, as seems to happen with some cancer drugs)

But by insuring the drugs, you in a sense reward high prices, and incentivize others to invent expensive drugs also rather than look for ways to do things cheaper.

In a way it reminds me of the debate that Charles Murray used bring out on welfare for mothers with dependent children.

If you give generous welfare, you make some lives better.

But at some point you reward mothers for being single, as the government check does not come with a less reliable entity called a husband.

And then you get family breakup, all caused by what has been called misplaced compassion.

With drugs, you could break the price fever by withdrawing insurance.

However, some persons would die sooner, and that as they say would ‘go viral.’

Bob – We could also ask what most people think is a reasonable price to pay for comprehensive health insurance with a deductible between $500 and $1,000 per year if there were no Medicare, Medicaid or ESI. My guess is between $75 and $100 per month which is similar to auto insurance. At that price, they might even be pleased if they never had to use the insurance because it would mean they remained healthy. I suspect, however, that there wouldn’t be nearly as much innovation especially in the specialty drug space. If the entire population of 320 million paid $100 per month for insurance, premium revenue would be $384 billion per year. That’s about 11% of current healthcare spending in the U.S. How the heck do we square that circle?

For most countries, the percentage of GDP a society is willing to spend for healthcare is a political decision in the end and is not necessarily related to how much healthcare its citizens want or even need. There are many worthwhile priorities both public and private and healthcare is just one of those priorities. It has to compete for resources with other priorities.

In America, drug companies want patients to pay little or nothing for their drugs but they want payers to pay through the nose. While they need to earn enough profit to provide their investors with an adequate risk-adjusted return on their capital after accounting for research and development failures as well as successes, a balancing act needs to be struck somehow between satisfying investors without bankrupting society.

At some point, we have to say enough is enough. I would prefer to see that happen by payers just saying no to covering drugs they deem too expensive relative to the benefit provided as opposed to government stepping in and dictating prices like it does with Medicare and Medicaid. For the relatively few individuals with lots of money, they will remain free to spend it any way they choose to including on expensive drugs and other medical treatments.

“But by insuring the drugs, you in a sense reward high prices”

You got it again. Those high prices remove resources from those unknowns (far greater in number than the known sick) so that in reality we are treating less disease not more.

Let me provide a follow-up on the cost of Lunesta. Originally the person we were helping had to pay up to $333 for the drug. Then we found discounted medications from GoodRx and Blink. Today we composed the appropriate letter to the insurance company to make them accept the fact that Lunesta was required. The price is now $7.35.

This works for me, Barry and probably everyone on this list. Unfortunately many of the most needy don’t have the resources or the knowledge to actually go through this rigmarole so very frequently they are the one’s that pay full price. What we are seeing in this area is welfare for the rich that want more security than the poor who don’t get the security. That is why when I talk about Barry’s protecting his country club buddies that is what I actualy believe is happening.

I should have added to the above that all these quirks demonstrate why Part D should never have been passed. I am shocked that a somewhat libertarian organization gave any support to Part D.

Allan, it wasn’t going to pass so they kept the vote open and beat a bunch of conservatives over the head with tax-free HSAs for everybody under 65-years-old and they got the votes to pass Rx in Medicare. That is how the MSA was turned into tax-free HSAs.

The MSA was going to be sunset so thank goodness for old peoples drugs.

Like I said, Rx in Medicare was the price we paid for tax-free HSAs.

I know the history real well, but many libertarian leaning conservatives believe that Medicare Part D is a good program. It is neither libertarian nor a good program. It is another entitlement program that attracts votes.

If you want a hard assignment, try running a public or a private insurance operation with this goal………..

“just saying no to covering drugs they deem too expensive relative to the benefit provided”

(in Allan’s words)

I am not saying this is a bad goal, in fact I think it is a good goal.

A lot of Americans take an absolutist position that preserving life is all that matters, no matter how short a time it is preserved for. Few of us will say in public that the attitude that death is just inevitable so why spend billions to prevent it. Nor are we allowed to say in public that some lives are so wretched that almost any extra spending is excessive.

One of my fantasies is that medical providers would be totally welcome to spend billions saving lives, but only so long as they do with their own money. Not the public’s money, and not the family’s money.

The Mayo Clinic and similar places have very large financial endowments. Let them do anything they wish with their own funds. Let them figure out how to pay for super expensive specialty drugs. If you prescribe it, you pay for it.

Bob — The good news is that a far higher percentage of the population, especially among the elderly, has executed a living will or advance directive or a POLST as compared to 15-20 years ago. Most of those people opt for no heroic measures beyond comfort or palliative care.

There have been cases, however, where doctors ignored the documentation and provided heroic or even futile care when the patient didn’t want it. They called it erring on the side of life. In those cases, providers should absolutely pay for the care or at the very least write off the cost and not expect any payment from the patient, the family or the insurer.

The bad news is that even those that are signing living wills are getting treatments today that keep them alive even longer at much greater cost. Living wills generally deal with true end of life scenarios that I don’t believe make that much of an economic difference.

1)Very few people are willing to cut their lives significantly shorter.

2)Many having living wills die before the will is even considered.

3)If the living will is considered I don’t know how much is actually saved. We are talking about the end of life where there isn’t much more to be offered.

4)When there is no living will we still let lives end.

5)In my own practice I didn’t see much difference between those being treated with and without a living will except when the ambulance arrived at the door.

6)Hospice IMHO has had a more important effect, but I don’t know if it has cost money or saved money.

We cannot assume that the physician or family know what usefull life there is for a patient when one considers ending a life that has not reached its endpoint. In a study some years back both the physicians and family were wrong as many times as they were right.

“There have been cases, however, where doctors ignored the documentation and provided heroic or even futile care when the patient didn’t want it. … providers should absolutely pay for the care”

That is a pretty definitive statement with a directive as to payment of costs that I find abominable. We are not always sure what the patient wanted and when the patient cannot answer for himself we have to use his agents. Sometimes the agents aren’t honest and have personal motives in mind. You think things are clear cut, but they aren’t. Once again you are blaming doctors with a broad brush.

So how common do you think it is for patients whose prognosis is dire and the prospect of recovery is zero are being given PEG tubes and vents so they can languish for weeks or even months in an expensive ICU bed? Isn’t that costly futile care that’s probably much more common in the U.S. than elsewhere? How common is it for patients with advanced Alzheimer’s or dementia to get an expensive surgical intervention or to be given drugs for everything from BP to cholesterol management to diabetes management when their quality of life is gone? If such patients have documentation that says they don’t want these interventions, that’s a good thing both for them and for society in my opinion.

THE BLAME THE DOCTOR GAME A LA BARRY BY CONFLATING DIFFERENT IDEAS:

“prospect of recovery is zero are being given PEG tubes and vents”

I get it Barry. You believe that physicians are conspiring together to keep patients on ventilators and PEG tubes. There may be a few crazies out there and thus you go on a witch hunt to blame the entire medical profession. The families, nurses and aids must be so scared they keep their mouths shut or your paranoia leads you to believe they are all in cahoots with the medical profession to establish vegetable gardens and reap the profits.

Families are an integral part of the decision making and they are generally the one’s frequently promoting that type of care. Of course, sometimes a demented patient breaks a hip. Would prefer them to writhe in pain? I guess should that demented patient (we won’t go into the different grades of dementia) develop appendicitis you would push for a rule to give him a lethal injection.

I blame the families who can’t let go especially when there is no documentation outlining what care the patient wants and doesn’t want if he can no longer communicate. Our litigation system also pushes providers in the direction of providing more care rather than less to reduce the risk of being sued. That’s unfortunate. It’s not about doctors or hospitals trying to maximize revenue. It’s about systemic impediments that prevent them from applying common sense depending on the circumstances. That’s what needs to change. At the very least, the more people we can convince to execute documents and make sure providers have them when they need them would be helpful to everyone including from a cost standpoint.

“I blame the families”

I don’t try and blame people for the policies that have been created by others. One should have a bit more compassion for those that are losing a loved one. That is a time people are not always logical.

But, before you blame the families you blame the doctors. Everyone is to blame except those that create social policy which complicates everyone’s life. You are even blaming the lawyers that are doing their jobs. When do you stop blaming people?

“It’s about systemic impediments that prevent them from applying common sense depending on the circumstances.”

Those systemic impediments are things that you support and promote on a daily basis. In the 70’s I had the luxury of still dealing with real people directly. By the time I retired I was dealing with your type of medicine which meant the patient was secondary to the government. …And now you complain about what you see?

“the more people we can convince to execute documents and make sure providers have them when they need them would be helpful to everyone including from a cost standpoint.

Where is your proof of the savings? You don’t have any real proof other than an abstract proof that deals with very limited variables making your proof useless. I’m pretty knowledgeable in this field and I don’t have a living will. I guess that is because I am an old-timer and don’t have to rely upon government to know when to live and when to die.

“One of my fantasies is that medical providers would be totally welcome to spend billions saving lives, but only so long as they do with their own money.”

In a strange way I agree. If that were the law physicians would not be treating patients and no physician costs would be created. I guess at that point the patient and doctor could sign a contract outside of the law where the patient paid the doctor for the doctor’s services. Thus cash payment has been invented. 🙂

Barry, your comments are focused on potentially futile care.

Although I am not an MD and have no first hand knowledge, my suspicion is that this type of care is not our greatest challenge in health care cost control.

What troubles me is the care which is NOT futile, but actually works in most cases and yet is just too darned expensive.

A 75 year old may well survive a heart transplant at a cost of $600,000.

Now step one before any difficult rationing is to see if the real cost is $600,000. What portion of that cost is a drug company getting very rich, or a hospital covering some extra overhead?

Then, if the cost is really is $600,000, is it time to ask whether we can spend that much public money on anyone, whether they are a symphony musician written up in the New York Times or a prisoner in the sex crimes unit in Moose Lake MN.

Bob — I don’t have as big a problem with the heart transplants as I do with the expensive cancer drugs that may only give a patient an extra few months of low quality life.

John Bogle, the founder of Vanguard, got a heart transplant at age 67 and is still going strong at 84. Former Vice President, Dick Cheney, was near death until he got a heart transplant at 71. He’s still with us as well after 20 months on the waiting list and using a LVAD to keep him alive.

At least organ transplants have elaborate protocols that determine who gets them and who doesn’t because there aren’t enough to go around. Anyone and everyone can get an expensive cancer treatment as long as there is a payer to pay for it.

Some people suggest that we use age-based rationing so that if you’re, say, over 90, you’re an automatic no code unless you can pay for your care yourself. I don’t support that either. I do think it’s unfair, though, that drug companies go along with price controls in other countries because they know they can make it up by charging what the market will bear in the U.S. market. Other first world countries are free riding by not covering their share of R&D costs. That needs to change in my opinion.

“with the expensive cancer drugs that may only give a patient an extra few months of low quality life.”

Barry, why should you be upset at persons living a few extra months? You support systems of involuntary pooling and then complain when patients aren’t willing to die or physicians aren’t willing to deny them future life. You blame both of these groups for high costs, but the fault lies in the policy that you support.

I remember my residency days when we were trying to treat all sorts of leukemias. The survival rates were atrocious, but we built upon the survivals learning how to extend the time interval of life until some of those cancers were cured. I guess in your world this should never have happened.

“organ transplants have elaborate protocols … Anyone and everyone can get an expensive cancer treatment”

In other words it’s OK to live for 6 months with an organ transplant, but not 6 months with cancer treatment? I guess you like the protocols because government can have a bigger footprint.

“I do think it’s unfair, … they can make it up by charging what the market will bear in the U.S. market.”

Yet at the same time you strongly support Part D where liquidity constraint has been muted. That helps the pharmaceutical companies make up the money on the backs of the US taxpayer.

“but the fault lies in the policy that you support.”

Other first world countries exert considerably more government control over their health insurance and healthcare systems that the U.S. does. Yet, they don’t have the same issues related to end of life care and excessive litigation that we do.

The issue isn’t policy; it’s culture. The culture in America is I want what I want when I want it and I expect someone else to pay for it. In other first world countries, it’s we don’t impose unreasonable costs and expectations on our fellow citizens. That’s a huge difference.

While we hear about long wait times for non-life threatening procedures in Canada and the U.K. we don’t hear about them in Germany, France, Switzerland, Sweden, Japan, etc.

Even if our healthcare costs were 30% lower than they currently are as a percentage of GDP, millions of people still couldn’t afford health insurance on their own, especially if they can’t pass underwriting or are older than 50. Huge numbers of people would have to be subsidized while Medicare and Medicaid would still be part of the system with the government rules and regulations that go with them. I don’t expect cultural attitudes to change anytime soon.

“Other first world countries exert considerably more government control over their health insurance and healthcare systems that the U.S. does.”

Who has the oldest continuous constitution? The United States, not all those other countries. Should we have followed their examples and created a monarchy?

Who would be speaking German if it weren’t for the United States entry into WW2? The other countries.

I am not saying the other countries are worse than America, they aren’t. They have good ideas, but your logic, because these countries do something, it therefore it is a good idea for Americans forgets history and forgets how the United States is the leader in free government, raising the standard of living all over the world, trade and wealth production, not to mention science including the healthcare sciences. Our ideas behind freedom and free markets must be working. Your ideas have been total failures in many countries and demonstrate a lack of sustainability in the present.

“The issue isn’t policy; it’s culture.”

If it’s culture then one must remember Alexis de Tocqueville who wrote about American Exceptionalism and its likely causes. We were different than the monarchies of Europe. That is a major part of why we grew to be so great, but the culture you promote is quite the opposite of 19th century exceptionalism.

The socialists are the ones that “impose unreasonable costs and expectations on our [Their] fellow citizens.”

“Even if our healthcare costs were 30% lower than they currently are as a percentage of GDP, millions of people still couldn’t afford health insurance on their own”

That is why insurance exists, but you promote a phony type of insurance so that it becomes unaffordable, overly complex and frequently unusable. If we were to practice the quality, liability, access of these other nations our costs would fall as well. Remember, building into our costs are the research and development that others copy or take at lower prices because those in power would like to see an end to American exceptionalism.

We can have our healthcare good, fast or cheap. Pick any two. If we want it good and fast, it will be expensive especially in light of the cultural headwinds of litigiousness and defensive medicine along with aggressive end of life care as compared to other countries. Throw in the high student loan debt that most new doctors, NP’s and even nurses enter their profession carrying and salaries need to be higher than they would otherwise need to be if that debt burden weren’t so onerous.

I don’t think getting rid of third party payer / ESI and moving commercially insured people into high deductible health insurance plans paired with a Health Savings Account will make a meaningful debt in U.S. healthcare costs. The headwinds outlined above will all still be there.

“We can have our healthcare good, fast or cheap. Pick any two.”

The real statement is that there are three components to healthcare. Quality, access and cost, but you can only have two of the three. In other words one should expect that any positive alteration of 2 out of the 3 components will cause a negative effect on the third.

“I don’t think getting rid of third party payer …”

What can I say, but you are dead wrong.

Your headwinds are partially a result of third party payer and If we had a true marketplace in healthcare which means getting rid of all third party payers (including Medicare, Medicaid and the VA) while permitting a free marketplace the savings would be huge.

Medicare alone would have saved a huge amount in just my practice. I remember when I would charge for doing outside labs. The total bill to Medicare for the lab was $20 to $30 for an annual physical. After the law passed preventing me from doing so the prices sky rocketed and the Medicare was paying the lab around $40 to $60 while I started an in-house lab that cost Medicare < $20.

With managed care most practices increased their overhead tremendously say from 25%-35% to 40% to 60%.

In hospital procedures such as colonoscopy cost double than for outpatient surgical centers. More recently physicians bought up by hospitals are having their fees reimbursed at much higher levels.

Dermatologists that were removing many items from the skin stopped removing them all at once and started to remove them on different days to maintain a higher reimbursement. They also would limit the area treated to what was approved even if other things were noted at the time of the initial visit. The patient would have to get new approvals and return.

Marginal medical care, one of the biggest cost factors, increases as the patient is divorced from the costs.

Medicare HMO's according to the GAO were paid around 1/3 too much when risk was factored into the calculations.

Today many doctors are estimating the extra time spent dealing with EHR’s to be in the vicinity of 15-25%. That is approximately the equivalent of a 15-25% rise in hourly costs for physician bills.

Physical therapy is not needed for many patients yet it is included in their outpatient costs.

Durable Medical equipment is higher than it needs to be because of a lack of a true marketplace.

Tremendous amounts of money is spent simply on gaming the system.

I have just provided you a small smattering of costs in no specific order that are increased because a true free marketplace doesn’t exist in healthcare. You can believe whatever you want no matter how foolish that might be.

Correction: make a meaningful dent in U.S. healthcare costs, not debt.

Allan, I think you overestimate how much more sensitive to cost people would be if they bought their own health insurance policy. Very few people would buy a policy with a deductible above $5K and once they needed something expensive that cost well beyond $5K, they would not be sensitive to cost after meeting their deductible.

Plenty of people wouldn’t be able to afford insurance and you don’t speak to how subsidies would be structured or how comprehensive a plan the subsidies would help pay for. Also, what happens if people lose their job and source of cash flow and can no longer afford to pay their premium? I don’t have a problem if 15% of the population that has few assets to protect doesn’t buy car insurance, assuming they have a car. I can buy car insurance that will cover medical costs and property damage if I’m involved in an accident whether it’s someone else’s fault or not. I’m not comfortable if 15% of the population has no health insurance just because they can’t afford to buy it.

In any given year, less than 4% of healthcare costs are accounted for by the healthiest 50% of the population. The sickest 1% of the population accounts for 20%-25% of costs. Whether they have insurance provided by an employer, Medicare, Medicaid, VA coverage or individual market coverage they bought themselves won’t make any difference to speak of in what care they get and where they get it if they need an expensive surgical procedure, cancer treatment, organ transplant, expensive specialty drug or other high cost care. These are the events that break the bank. Primary care doesn’t cost all that much even if there is some waste attributable to third party payers.

Finally, I don’t see how private insurance policies can be structured to not cover marginally useful care in exchange for a lower premium because you can’t define it with precision and it can vary widely from one person to another. You might be able to offer a lower premium for people who will agree to settle disputes through binding arbitration or health courts but I don’t think doctors will change their practice patterns for patients that choose those options vs. patients who don’t. Instead, they will practice in a consistent manner across their entire patient panel. Also, even if everyone bought their own health insurance policy and there were many competitors in the market, insurers will pay most of the bills in the end. That means they will impose whatever documentation requirements they think they need to impose and those rules will vary from one insurer to another. Doctors will still find it frustrating and I doubt their overhead will decline much from what it is now unless they are in an area where people are prosperous enough to self-pay which would allow the doctor to not accept any insurance. It won’t work in most places.

Barry, you are always WRONG. You spew, “Very few people would buy a policy with a deductible above $5K” NOT TRUE. When a 30-year-old couple and 2 children have $9,000 Trump age-based tax credits to purchase personal, portable and permanent HSA Qualifying Individual Medical (IM) for $4,500 a year and have President Trump deposit $4,500 in their HSA, TAX FREE, with a $6,000 deductible, per person, that pays 100%, MILLIONS of young families will flock to that option.

BUT, my agents will say – EVERYBODY and their DOG is getting the ONE deductible $13,100 FAMILY deductible because it drops the premium $1,000 a year which makes your HSA deposit rise to $5,500. Most think they are not going to get anything with a $6,000 deductible anyway so they might as well go higher and get another $1,000 in America’s BEST tax dodge, the tax-free HSA.

BUT, BUT, BUT, they are all getting the new kind of LIFE insurance that pays $190,000 CASH for CANCER, heart attack or stroke. TRUST ME, you get cancer you will need tons of CASH to pay 2 years of deductibles, wigs and all of the lost wages. It is only $67 a month, should I show you how that works?

Prospect says, “Is that $67 apiece?” My agent says, “NO WAY JOSE, that’s for BOTH of you, should I show you how that works?”

TRUST ME, Barry, they will get whatever I tell them to get. WHY, because I’m a salesman with tricks.

DEVON, I’m looking at the sales material from 2004 that says that TIME was the 1st to market Medical Savings Accounts and the company, FORTIS, was the 18th largest company in the WORLD doing $4 billion NET annually. So either FORTIS is WRONG or you DEVON are wrong.

They write, – The ONE DEDUCTIBLE Plan. It’s the smart, simple, economical way to look at heath insurance.

ECONOMICAL – For Webster’s, economical means careful, efficient use of resources. For Ron Greiner, economical means One Deductible. The money you save on premiums can more than pay for your routine health care expenses. If the unexpected does happen, you’re protected from financial hardship – that’s what health insurance is for. Mr. prospect, am I going too fast for you?

DEVON, FORTIS would NEVER make a mistake and LIE. So somebody is a FRUITCAKE here.

https://www.youtube.com/watch?v=wneCa_yIuzg

“Allan, I think you overestimate how much more sensitive to cost people would be if they bought their own health insurance policy.”

Firstly you neither have clinical proof or empiric proof to back up what you are saying. Let me answer you with just one example of the many mentioned earlier. We can go example by example until you get the point and I can add almost an unlimited list of examples. You don’t bother responding to examples for that would prove you to be totally wrong.

Do you think that patients without a special need would pay almost double to a hospital for a colonoscopy if they were paying OOP? Wouldn’t those people mostly opt for a less expensive insurance plan that wasn’t so generous? Would they pay for marginal care? Maybe you would because you and your country club friends have a lot of money, but others are struggling just to keep a roof over their heads.

We don’t know how high the deductible would be in a free market though you attach all sorts of numbers to the issue. From where do you divine such numbers for a future free market system?

“they would not be sensitive to cost after meeting their deductible.”

How do you know what would happen in a free market? Have you suddenly ascended from being a mere human to becoming a prophet? Free markets innovate, something that seems to scare you. For all you know the insurers might rebate money to those who obtain their care using less expensive alternatives. You draw pat conclusions because you are locked into government care and are unable to think in an innovative fashion.

In a free market prices would fall and so would insurance rates so more people could afford insurance and more people could afford higher deductibles or co pays which leads to even lower insurance costs.

We have subsidies today for the 15% you talk about and we would have subsidies for them tomorrow if a free marketplace existed. The only difference is that the insurance costs would be lower so the amount of subsidies needed would fall, taxes would fall and more people would be able to buy insurance.

“The sickest 1% of the population accounts for 20%-25% of costs.”

This may be true but demonstrates that you do not understand the economics of healthcare. Many of the sickest people are not the sickest people the following year. What we are really talking about are the known high cost individuals and the unknown high cost individuals where the unknowns are much greater in number and carry normal priced insurance to cover the illnesses you are talking about. The unknown high costs are a great part of those 20-25% and if we remove Medicare and Medicaid then that known group dwindles to much lower numbers making your point near meaningless and most definitely counterproductive. You are copying the uneducated talking points of the socialists.

“These are the events that break the bank.”

In the free market the vast majority of those patients presently in third party payer involvement will be unknown high costs and will therefore be insured. The price differential and marginal care, both of which are very high, would radically fall.

“Finally, I don’t see how private insurance policies can be structured to not cover marginally useful care in exchange for a lower premium because you can’t define it with precision and it can vary widely from one person to another.”

That you don’t see how policies can be structured is not surprising because you are so focussed on government care rather than a marketplace. In the malpractice insurance company where each covered member had ownership, not only did we structure things to lower premiums, but we structured them so well the company was sold paying me a six figure sum while relieving me of a cost for my tail end which was a smaller six figure sum. Additionally, I had continuous insurance with lower than average premiums in one of the highest malpractice areas of the country. That is how innovation works and that never would have occurred if you were in charge.

You may not know how to do these things, but there are a lot of smart people out there that do. Unfortunately, you wish to tie their hands so that government care prevails.

“I don’t think doctors will change their practice patterns for patients that choose those options vs. patients who don’t.”

What do you know about what doctors will or will not do? Everything you say is based upon your personal preference and security. It appears you know very little about how the rest of the world thinks or acts and that is what counts.

“I doubt their overhead will decline much from what it is now”

Nothing you say on these issues is based on fact. Insurance has existed since I started practice. As the government involved themselves more and more my % of overhead increased by at least double.

I gave you a tiny smattering of specifics involving those things where the quick savings of a marketplace could occur. It is time for you to stop the generalities and handle every issue point by point. You can’t because you have little to no data and a lot of information that is totally wrong.

Allan, for Barry there is no cure.

Regarding just one point that Alan made —

it is an expensive scandal that providers get far more money when a procedure is done in a hospital or by a hospital-owned doctor, versus done independently.

But how hard would it be for Medicare to go to “site-neutral payments?” They could do it tomorrow morning theoretically, but there would be a ton of lobbying to keep excess payments flowing.

Makes sense. The same should apply to urgent care. If it were really more expensive for hospitals to provide urgent care via the ER, they would rapidly open up adjacent urgent care clinics in order to cut costs.

Although I don’t see how opening a separate clinic could be cheaper than utilizing surplus ER resources.

After the tax-free HSA is ENHANCE in the passage of Obamacare Replacement in the US House of Representatives everyone will wonder how did that happen with just 17% approval?

Then everyone will go bipartisan because of the tax-free HSA. The HSA looks like the only thing everybody can agree on, so that is nice. It is REPORTED: “A Missouri congressman is leading a bipartisan effort to allow tax-free savings accounts for buying fitness and sports equipment — including golf clubs.

It’s unlikely that low-income families would benefit much, Zaretsky said, because most of them don’t use health savings accounts.

Higher earners have been more likely to use the accounts, she said. That includes her brother-in-law, who she said disagreed with her on golf’s potential to improve physical fitness.

“But he doesn’t need that tax expenditure,” Zaretsky said. “He’s doing fine.”

Smith’s bill, introduced in March, had 19 Democrats and 12 Republican co-sponsors as of Monday.

He said he’s open to tightening the language to prevent fraud and abuse, if need be.

Andy Marso: 816-234-4055, @andymarso

Read more here: http://www.kansascity.com/news/politics-government/article146444549.html#storylink=cpy

For all the glorious cost savings that Allan claims we can get from a free market healthcare system, why have no politicians run on that agenda and WON? Medicare isn’t going anywhere and neither is Medicaid. Neither is employer sponsored insurance and the tax preference that goes with it. Heck, even the ACA’s Cadillac tax on high cost health plans was beaten back by lobbyists.

As for Health Savings Accounts, more and more employers are offering them at least as an option but I haven’t seen them make much of a dent in lowering healthcare costs. They are a nice tax shelter for better paid employees though and for people without employer sponsored insurance who can afford to fund them. Millions of people can’t afford to fund them, of course.

As for site neutral payments, I agree that Medicare should move in that direction. At the very least, maybe we can get price transparency with respect to hospital and ASC facility fees.

“why have no politicians run on that agenda and WON?”

This is Barry’s proof, absent of data, studies and logic, why a free market system won’t work. He forgets about all the questions asked and everything we know about human behavior. He forgets history and all the studies that have been performed even in real life. Barry has no answer because his ideology is faith based, much like religious beliefs except religious beliefs offer spiritual benefits while his ideology offers little more than being enslaved.

Medicare will not be touched for now by anyone, but it will be dealt with in the future, only the pain will be greater where the one’s paying for Medicare today don’t even have a guarantee it will be there when it is their time. I don’t advocate drastic changes in any welfare program presently because I think we should create a free market system with some type of safety net. We need to start with the rest of the population and then work the safety nets into that scheme.

People want things for free and if they don’t see where their money is leaking from they believe those things are free. There is pain associated with the free marketplace, but there is far more pain in a government run system where the system is pictured as a comfortable space that is not seen to be empty until the doors are locked shut.

Barry needs to re-watch the Wizard of Oz again and take a dose of reality.

Barry, you’re Socialist Spew is terrible. If the DNC and Hillary are paying trolls like you minimum wage they are overpaying YOU. YOU say, “As for Health Savings Accounts, more and more employers are offering them at least as an option but I haven’t seen them make much of a dent in lowering healthcare costs. They are a nice tax shelter for better paid employees though and for people without employer sponsored insurance who can afford to fund them. Millions of people can’t afford to fund them, of course.”

In the 50010 zip code, Ames Iowa, on 10/01/2017 a 64-year-old couple earning $65,000 a year has a choice. 1) continue to pay $1,952 a month with “Medica” and have a $6,850 deductible with $7,150 Out-Of-Pocket and have a $80 Co-Pay or Doctor Office Visit Expense (DOVE) The quarterly premium for 3 months is $5,856. OR

2). The Nation’s largest insurer, instead of little-bitty “Medica”, United Health Care’s (UHC) Short Term Medical (STM) with a smaller $5,000 deductible then 100% coverage for just $767.82 quarterly and save $5,088.18 in premium.

PLUS, the over-priced GUARANTEED ISSUE Medica’s deductible is too large for an HSA but UHC’s deductible is just right. If this couple deposits $7,650 in their tax-free HSA they save $1,530 in income tax (15% Federal + 5% State) which is DOUBLE the amount of the health insurance premium. Admit it Barry, that is affordable health insurance.

We will train the HSA salesman to say, “Listen to Paul Simon. Simon says, just set yourself FREE.” SERIOUSLY FOLKS, if you set yourself FREE you will have more money than you have NOW plus it’s like getting FREE health insurance with a smaller deductible. (Closing Question) That’s better than being poked in the eye with a sharp stick isn’t it?

Barry, it’s not MAGIC, it’s just MATH!

https://www.youtube.com/watch?v=vWPQQbldFjw

Of course, your 64 year old couple has to be healthy enough to pass underwriting to get the STM plan which many people that age can’t do. Moreover, I asked UNH last year how many STM plans it has in force. Answer: about 100,000. Between their fee based and risk based business, they have more than 30 million people covered by health insurance of which a measly 100,000 are on STM plans.

Separately, you, the great insurance expert, should know that for 2017, the maximum amount that can be contributed to a Health Savings Account is $6,750. That’s from the employer, if any, and the employee combined. Finally, it’s highly unlikely that very many 64 year old couples with income of $65K could afford to pay $1,952 per month for health insurance unless they had built up considerable savings or inherited money. Your cherry picked examples are just that: cherry picked.

Barry, U R A hoot. YOU spew, “Separately, you, the great insurance expert, should know that for 2017, the maximum amount that can be contributed to a Health Savings Account is $6,750.” Read’em and weep Barry:

May 9, 2016 – HSA holders can choose to save up to $3,400 for an individual and $6,750 for a family (HSA holders 55 and older get to save an extra $1,000 which means $4,400 for an individual and $7,750 for a family) – and these contributions are 100% tax deductible from gross income.

I am always conservative and correct, unlike you Barry. I assumed you knew about the catch-up clause for people over 55-years-old with tax-free HSAs.

So I am right and you are WRONG, again.

Health Savings Accounts are a good way to mitigate undesirable incentives present with tax-advantaged health insurance. Beyond that I don’t see what the big deal is. They’re certainly not a “cure for panacea and other ills.”

Bart, not only are HSAs a panacea but also the silver bullet.

I know you are a PRO with propaganda when you say that tax-free HSAs are not a panacea. This is not my 1st rodeo you know.

I have nothing against STM insurance being available for purchase, so long as it’s not tax-advantaged. But I wouldn’t have believed it could qualify as an HSA-compatible HDHP.

Why do you feel that way, Bart?

It’s funny that both the car insurance market and the home insurance market work fine without tax advantages or preferences even though both auto body shops and home repair contractors will pad bills when they know insurance is paying. At least both of those markets offer price transparency and the information asymmetry issue related to what work is needed and what isn’t is much less of a problem than in the healthcare and health insurance market.

Barry, you should be happy to learn what Blue Cross is doing to the health insurance agents that you hate. Blue Cross scams everybody and in Iowa they have the agent’s commissions down to $15 a family per month, $180 a year. How would you like doing customer service for dog food?

My friend from high school that sells home owners insurance in West Palm Beach has a boat that cost $2.3 million and he has a plane.

I’m not living comfortably being run out of business over and over again. I know Barry you think I’m overpaid. My beautiful wife is overpaid too and you think cancelling all of her renewals is perfect. Why should she have any money coming in right? She is working for $11 an hour now because who needs someone who did customer service on the oldest tax-free HSAs in America? She would of known that that 64-year-old couple could deposit another thousand in their HSA. She is a lot smarter than you Barry but that is an understatement.

If you like your plan you can keep your plan, PERIOD! – Prez Obama

On the whole there is no better person to make a healthcare decision than the patient. On average they can do it better and at lesser expense than Barry can for them or any high school drop out that might be in the U/R department.

People generally buy insurance on the free market and thus there is a lot of price transparency. Companies compete with one another and no tax advantages exist. The free market does a fantastic job except it has difficulty competing with the faith based religion of socialism. That is until a nation with oil wealth along with favorable landscape, minerals and access to the oceans, like Venezuela, runs out of other people’s money. Then they have to rely upon dictators while they starve unless they rise up and create what was created in this nation. Too bad that so many people like Barry wish to destroy the foundations that built our great nation.

Allan, The United States is a nation with laws: poorly written and randomly enforced. — FZ

Insurance is a contract between the consumer and the insurance company. The consumer should have legal rights that when violated they can complain to the State Insurance Department and they come down on the Insurance Company with both feet. The Insurance Companies must fear the State and fulfill their contractual obligations to the consumer. In a perfect world the consumer is KING.

In a rotten SOCIALIST world the State is the Insurance Company and when the consumer wants to complain who do they call? Who is the State afraid of? In a Socialist’s world the consumer is a SLAVE. In a Socialist’s world people have to get down on their knees of their heart and beg a politician for a handout in retirement. Socialism doesn’t work because people like to own stuff. — FZ

Medi-Share is a community of “Christians” who have agreed to live as the early church (Acts 2 & 4) when it comes to sharing each other’s burdens. WARNING:

THIS IS NOT INSURANCE

These “Christians” take away the consumers’ right to sue!! WARNING FLAG!! Their PRE-X goes back FOREVER, not just 1 year or 5 years. PRE-X conditions are covered after 3 years not just 24 months like insurance. AND, if the consumer wants to complain who do they call? The Insurance Commissioner is going to say, “Sorry Ma’am, this isn’t insurance so my hands are tied. Maybe you should try calling the Pope.”

These “Christians” are GOOD. They use the PHCS PPO medical network coast to coast. TIME Insurance Company (TIC) nurtured this PPO network at their beginning. It helps when you have FORTIS, doing $4 Billion NET per year, funding you.

It is still NOT INSURANCE and it is EXPENSIVE to have these “Christians” strip you of your legal rights. SALESMAN CLOSE: Seriously, do you really want to have no legal rights if your 9-year-old child has a brain aneurysm?

I’m high pressure and I don’t go back. Seeing these consumers 1 TIME is enough for me. I don’t email them a bunch of crap and become their pen pal either. If the consumer wants to have Medi-share I will respect their stupid decision and scream the 4 letter word — NEXT.

“Allan, The United States is a nation with laws: poorly written and randomly enforced.”

Z, that is true, but exists in all nations and compared to other nations we do pretty well.

“Medi-Share …THIS IS NOT INSURANCE ” Of course it isn’t traditional “insurance” Though the plans do utilize reinsurance.

The government forces insurance upon the individual to prevent itself from paying for unpaid healthcare bills. Medi-Share meets the burden. We shouldn’t be forcing health insurance down anyone’s throat in a free society. I don’t know that your contention that all their rights are lost is true. From what I have heard, many are well served by Medi-Share.

Just like looney Rooney at Golden Rule, a big NCPA donor so Devon says they enrolled the 1st MSA, they take away the consumers right to sue.

Golden Rule raised rates quarterly so those that paid quarterly never had the same rate twice. They also TERMINATED all children at a majority age where we had a Dependent Conversion Privilege (DCP) so all prospects with children were an easy sale.

My own son was diagnosed with Crohn’s at 17-years-old and he was on the same plan 3 years ago this month, at 31-years-old, when he had a $250,000 surgery.

That’s why I know losing your health insurance at 26-years-old sucks if you are diagnosed with MS like my daughter was at 24-years-old. All politicians love terminating insurance at 26-years-old, the fools.

whoah this weblog is magnificent i like studying your

posts. Keep up the great work! You know, many persons are looking around for

this information, you could aid them greatly. https://towyardcars.com/author/epifaniabat/