(A version of this Health Alert was published by Forbes.)

It would be fair to say markets were blindsided by the U.S. Treasury’s 300-page plus batch of regulations that blew up the merger between Pfizer and Allergan. The deal was widely described as a so-called “inversion,” a deal whereby a U.S. domiciled company reverses itself in to a foreign firm for the purpose of reducing its U.S. tax burden.

Pfizer has been trying to invert itself for a long time. It has not been easy. In May 2014, Pfizer gave up its dance with AstraZeneca, a British-based global pharmaceutical company. The problem for a huge biopharmaceutical firm like Pfizer is that it cannot just collapse itself into a foreign shell.

As I discussed in an article published in the wake of the failed AstraZeneca deal, the newly consolidated company has to have a minimum 20 percent foreign ownership to qualify for tax inversion. That means the target has to have a market cap at least 25 percent that of the U.S. bidder – and that is only if the deal is fully financed by equity. Not that many companies are big enough to fit the bill for a company like Pfizer.

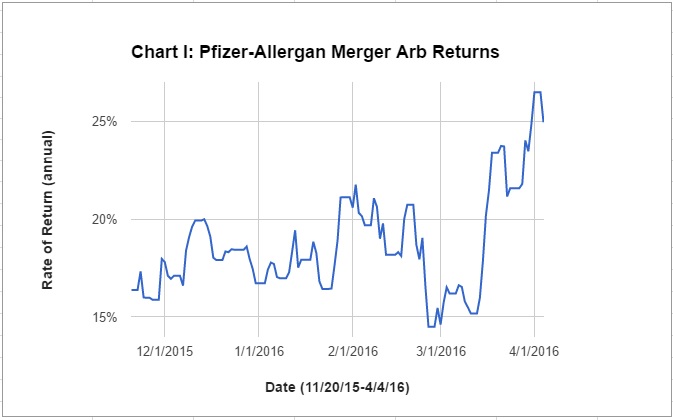

The deal with Irish-based Allergan was first disclosed provisionally on October 29, 2015, and confirmed on November 23. Since then the return to an investor who arbitraged the merger by buying one share of Allergan to exchange for 11.3 shares of Pfizer (the terms of the all-equity deal) ranged between 15 percent and 21 percent until March 17 (assuming one year for the deal to close, and taking account Pfizer’s February 3 dividend of $0.30. See Chart I.)

Not until after the middle of March did the spread widen to around 25 percent, suggesting something was indicating to investors they needed to demand a higher risk premium. Still there is nothing indicating Treasury’s regulations were leaked before being released on Monday and blowing up the deal.

Read More » »

(A version of this Health Alert was published by Forbes.)

(A version of this Health Alert was published by Forbes.)