Medicare Advantage

Uwe Reinhardt had a column the other day in which he argued that:

- We are paying Medicare Advantage plans more than we pay for similar patients in traditional Medicare.

- Enrollees in traditional Medicare are paying higher Part B premiums in order to subsidize the higher MA payments.

- This is bad public policy; we should instead have a level playing field for subsidies for both programs.

Now here is a surprise: I agree with Uwe.

Here’s a second surprise: I bet if they could get a real level playing field, the health insurers that offer MA plans would agree as well.

But Congress has not been willing to allow this. Politicians don’t just interfere with overall payment rates, Congress actually gets into the weeds and dictates payment rates on a county by county basis. The reason: to protect vested interests in the districts members of Congress represent.

Here is what I don’t understand about Uwe’s column, though. You might expect people in a fox hole to discuss many things, but you don’t expect them to ignore the fact that bullets are flying overhead. Similarly, if you are going to write about Medicare and Medicare Advantage payment rates, it’s hard to understand why you neglect to mention the tsunami that is about to hit both programs.

Tsunami

Over the next ten years, about half of the cost of ObamaCare ($716 billion) is going to be paid for by reduced spending on Medicare. And it doesn’t end there. The real per capita growth rate for Medicare has been set in the Affordable Care Act at a rate a little higher than the real per capita growth rate for GDP, indefinitely into the future. In other words, Medicare is going to grow at approximately the same rate as our income.

Think for a moment about what that means. In one fell swoop, President Obama and the Democrats in Congress actually solved the problem of escalating future Medicare deficits. If Medicare grows no faster than our income, then the financial burden of Medicare is never going to change. We can keep doing what we are doing right now, forever. (And I should add that the Republicans, through the Ryan budget, have signed on to the same growth rate!)

So why isn’t everybody out celebrating? Why isn’t there dancing and singing in the streets? Why aren’t church bells ringing, bands playing, dogs barking, etc.? Why is there so much gloom and doom? Why is everybody talking about the problem if the problem has been solved?

Answer: because although there is a law that restricts Medicare spending, there is no law that restricts overall health care spending. We’ve imposed a global budget on health care for the elderly and the disabled, but we’ve imposed no global budget on anyone else. If the past is a guide, per capita health spending will growth at twice the rate of per capita income, in real terms — meaning that Medicare rates will fall increasingly behind the rates paid by all other payers.

Now in recent years the growth rate for health care spending has slowed. And it may continue to slow. But, and here is the important policy point, whether or not it slows we have created a global budget for seniors that doesn’t allow their spending to track everybody else’s spending.

Here is what I previously wrote at this blog:

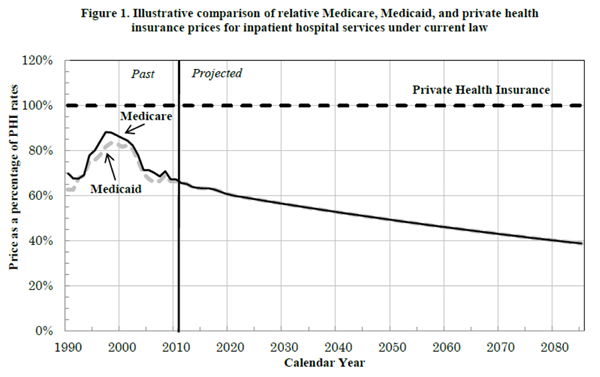

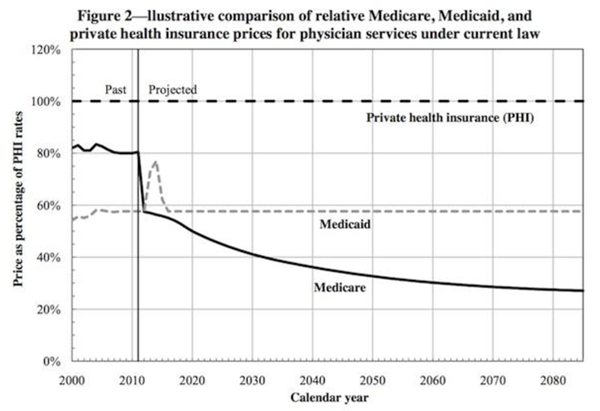

Look at the graphs below, taken directly from the Medicare Office of the Actuary’s memorandum in response to the 2012 Medicare Trustees report. In about two years, Medicare payments to doctors will fall below Medicaid rates and will fall further and further behind Medicaid with each passing year. Medicare payments to hospitals will basically match the Medicaid rate, indefinitely into the future. What will this mean? For one thing, seniors will be lined up behind the welfare mothers in the attempt to find doctors who will see them and institutions that will admit them. As Harvard health economist Joe Newhouse has explained, seniors will likely have to seek care at community health centers and safety net hospitals. As the Medicare Office of the Actuary has explained, in a few short years, hospitals will begin closing and senior citizens will have increasing difficulty obtaining access to care.

The tragedy is that outside of Rick Foster, Joe Newhouse and a few people associated with the NCPA, no one is talking about this. And in saying that Uwe is ignoring the tsunami, I don’t mean to imply that is unusual. What is about to happen in Medicare is being ignored by almost everybody — by Capitol Hill, by the health care media, and by almost everybody else in the health policy community.

There is one other thing that is being ignored — and this is where Medicare Advantage shows real promise. The administration has been spending millions of dollars on pilot programs and demonstration projects for the purpose of discovering how low-cost, high-quality care can be delivered. And three Congressional Budget Office reports (see here, here and here) have found that these programs are not working.

Yet there are places where similar techniques are working and in many cases the innovators are the Medicare Advantage plans. That’s right. Despite President Obama’s wish “to find out what works and then go do it,” the health plans that are the most entrepreneurial and the ones that are showing the most impressive progress are the very programs that the president campaigned against as a candidate and for which funding is scheduled to be cut by the Affordable Care Act.

Go figure.

“In a few short years, hospitals will begin closing and senior citizens will have increasing difficulty obtaining access to care”

Ah yes, of course one of the many unintended consequences of ACA.

This is not an acceptable solution when it comes to caring for our nation’s elderly. Creating more barriers for senior citizens to obtain quality health care is an irresponsible move from our government.

We can’t afford to provide unlimited care for everyone. Under a “socialized” system, eventually there comes a point where you have to start cutting costs (i.e. cutting old and sick people). This is just a step in that direction.

It’s just expediting the process of putting grandma and grandpa into the grave.

OK, but let’s not ignore the savings that can be secured by cutting the young and sick people.

Death panels?

I didn’t want to come right out and say it, but, yes, you are on the right track.

It is a shame that Capitol Hill and health care media take the approach of “ignorance is bliss” once these issues start to pop up.

Get your umbrellas ready for the tsunami that will throttle the nation’s medicare programs

Medicare is a pretty bad program, so we shouldn’t mourn to much, but this isn’t the way to fix it.

“Medicare is a pretty bad program”

Yes Dewaine, it is. Which is the primo reason that seniors need MORE choices, not fewer.

It’s up to the government to make Medicare better but they have shown no interest in doing that. Instead the government chooses to attack Medicare Advantage plans – which are very popular, having voluntary enrollment of nearly 30% of the Medicare-eligble population. The government thus chooses to stifle competition rather than stimulate it. . . and with no competition, plus the power to destroy any competitor, the government has no incentive at all to “fix” Medicare.

Seniors take care of yourselves.

Let’s face it, an umbrella ain’t much good in a tsunami. Get ready to drown.

I don’t think that they are nearly as ignorant as they all act. “Ends justify the means” is more like it.

It is highly irresponsible to cut funding from the health plans that are showing the best progress, and continue to fund programs that are obviously not working.

It makes you wonder what they really want.

“That’s right. Despite President Obama’s wish “to find out what works and then go do it,” the health plans that are the most entrepreneurial and the ones that are showing the most impressive progress are the very programs that the president campaigned against as a candidate and for which funding is scheduled to be cut by the Affordable Care Act.”

Do we really expect any different? It’s all rhetoric.

You are right. Everybody is ignoring the tsunami.

The traditional Medicare program exhibits perverse incentives. Ironically, I sort of like the original design of Medicare Part D (drug plans). The much derided Donut Hole was designed to make the plans appealing to a wide range of seniors by holding premiums down so even healthy seniors would find the plans valuable.

Basically, everyone had a small deductible (about $300), everyone with spending above the deductible got a significant benefit (i.e. 75% subsidy) until they reached spending of around $2300. Then seniors would bear all the costs until their total drug expenditures surpassed around $5300, at which time seniors had 95% coverage.

Unfortunately, the PPACA basically did away with these incentives that encouraged seniors to ask for generics and track spending so they would not reach the donut hole.

I agree Devon,

The only medication coverage for seniors without employer coverage was limited to about $2000.00 per year.

Part D provided cost sharing and was well designed to promote cost sensitivity while transferring risk.

Taking away the donut hole will, already is, causing less affordable prescription options as copays go up and formularies drop expensive drugs.

Seniors are getting slammed already.

Janice

I once co- taught a health care course with Bill Frist, fresh out of the Senate.

In front of the students, and anticipating Devon, I scolded him for having too low a deductible in the MMA 03 Part D deal, which forced them to put in tHe donut hole.

He got up and told my students: “You have now seen brilliance in action. That is what economists are: brilliant. But eh have no common sense.”

He then told us how laws are written, and how it was important for the Bush administration to have a lot of seniors benefit from Part D in the first year.

So, yes, Devon. that is how politics works.

The alternative would have been to leave drugs not covered by Medicare, and then John would write angry posts how inefficient that is, because of d substitution effect.

If it is a choice between having John angry or laying more taxes — actually incurring more debt, because the MMA 03 was not financed — I take the latter.

What Frist dismissed as political sounds like good marketing — creating a product that a broad ranger of seniors would want and benefit from.

I’m a little surprised we haven’t seen exchange plans designed like the original Medicare Part D. One problem the Administration and insurers have is that young people aren’t signing up in droves. A donut hole would be a way to make the plans affordable, while providing a benefit that younger people would find of value.

For that matter, Medicare Advantage plans that feature a coverage gap (i.e. donut hole) with a built-in HSA/HRA would be a good idea.

But does anyone really expect Congress and whoever is in the White House to actually hold to those growth rates in Medicare? I certainly don’t, and never have.

Yancy Ward, you have made the point that is missing in John’s argument. There is no political will to execute the cuts; hence, the doc fix every year.

The doc fix needs to happen or there will be a large scale exit of providers from medicare. As providers all we are waiting for is a permanent change. Someone needs to have the courage to fix the flaw that was written into the law back in the Clinton years. The uncertainty is what we in the healthcare deliver field are so worried about. Make the change and we will then know how to adjust our practices to still remain solvent. May be dropping medicare, may be going to completely private pay but if someone could just make a decision that would help. Do not expect one however. I think this administration wants to keep everyone on edge so that they can scare people and tell them that “if you think it is bad now, just wait until the conservatives get their way”.

John:

You may not realize it, but there is a word limit on posts for Economix. Much as I would like to, I can’t discuss the world in a given post. The world limit prohibits it. So there’s your answer to why I did not go into the point you raise.

I think the issue you raise is a serious one. Having served on the Medicare Technical Advisory Panel that advises the actuaries of CMS, I am well familiar with the long-run implications of the ACA on Medicare. No one believes that these strictures would actually be observed if private health spending galloped ahead at a faster rate than GDP. In other words, no one I know is that stupid. After all, we have the SGR as a model.

I did raise this issue, by the way, in commenting on Paul Ryan’s initial Medicare reform proposal in the 2010 budget passed by the house. He had proposed to index the defined contribution to Medicare by only the CPI growth, not an index of health spending growth. I thought that might not be sustainable without effectively turning Medicare from a middle class to a poverty program.

I am sure you raised the same alarm you raise over the ACA then, too, and would love to see your post on it.

Best,

Uwe

Uwe: First I tried to talk Ryan out of it. But when that failed, we did not back away on its implications. Tom Saving and I wrote this editorial for the Wall Street Journal and included a graph so that everyone would know what we were talking about: http://online.wsj.com/news/articles/SB10001424052702304066504576345732775990392

Uwe and John,

We COULD have something like the Ryan plan and not turn Medicare from a middle class program to a poverty program IF the government got rid of price controls. Then the payments set by CMS would not be the only compensation the doctors and hospitals could get. In other words, let the hospitals and docs set their prices. If the government pays $60 for a doctor visit and the doctor wants to charge $100, the patient comes up with $40, either out of pocket or with supplementary insurance.

That one reform would also have great incentive effects on both the demand and supply sides.

What do you both think about that idea?

I think that is a terrible idea. Alas, I am just off to the UK and can’t explain why it is a terrible idea.

I think the deal should be between the MA health plan and the Medicare beneficiary, whatever that may be.

David: I like your approach, but I don’t like restricting Medicare spending to the CPI when health care spending in general is growing at GDP (real) Plus 2%. Tom Saving and I have suggested reforms that would slow down the growth of all health care spending and your idea of balanced billing (for some patients) was one of them. See:

http://healthaffairs.org/blog/2011/11/15/a-better-way-to-approach-medicares-impossible-task/

I wrote a very thorough examination of Medicare Advantage in December 2009 and most of it still stands (http://tinyurl.com/onwmcfk).

The final paragraphs recommend:

Setting MA benchmark equal to average or minimum (or somewhere in between) bid in each county, but include traditional Medicare (i.e. government) as a bidder. In counties where traditional Medicare is above the benchmark, patients pay the difference.

Allowing MA plans to reduce costs by increasing deductibles, co-pays, coinsurance.

Wrapping health-status insurance (as per John Cochrane) around MA, instead of zero-based contracting annually. (As explained in the paper, I propose this by combining the best of Medigap with the best of MA.)

I have been advocating this for many years. As well as to eliminate insurance contracting and networks – Just have the insurance companies publish a fee schedule and pay any licensed provider that fee. Most people think healthcare is a commodity – all providers are pretty much equal. We all get paid the same so the service is the same. Having the ability to charge what we want and have the insurance company set the fee schedule they will pay will allow for quality competition. If my services are superior then people will be willing to pay the additional sum above what the insurance will pay. If I continue to offer the best service my practice will thrive, if not I will need to adjust my prices or die. Having the insurance companies limit every contracted provider to the same rate creates this commodity perception and does not allow me to truly compete on a quality basis.

Vince, why don’t you publish a list of the prices you will charge an uninsured patient? This would give consumers some idea of how you value the services you provide.

I don’t believe it would be legal for insurance companies to collude on a fee schedule,even to the extent of agreeing on 100% of Medicare or some other percentage.

I don’t know how old you are, but what you describe was how indemnity insurance worked in the 70’s. Then BS started UCR as payment in full and the world changed.

<>

John, I disagree with your statement here…the reason is infinitely more pathetic that the one you offer. The rates are set on a per county basis to recognize cost differences between rural and urban counties, as well as regional cost differences, but in actuality what creates vast differences between counties is the amount of Medicare fraud that goes on in various places. In South Florida our true healthcare costs in Miami are slightly less that those in say Palm Beach (borne out by the cost of private individual health care policies). The Medicare situation is however totally opposite.

It costs Medicare in Miami about $1,500 monthly per beneficiary to deliver part A and B services when it does so directly. Just 60 miles north, in Palm Beach, those costs fall to about $850 even though healthcare is a tad more expensive in Palm Beach…why ? Miami is the healthcare fraud capital of the world, whereas the fraud in Palm Beach is probably just at the national average. In mindboggling stupidity, Medicare reimburses Miami plans at the same ratio to their cost, as it reimburses Palm Beach plans, even though Medicare is quite aware that 1/2 of its reimbursement money goes to reimburse for the local fraud that Medicare Advantage companies (but not Medicare) already contain very effectively. This excess reimbursement is beyond insane, but it is the reason why Medicare Advantage plans in Miami routinely offer free full dental, zero copay for doctor visits, unlimited free transportation, and pretty much zero copay for most medical procedures. In contrast, MA reimbursements in Rochester Minn. run about $700 to 800 /month even though they have excellence in care . Plans there have higher copays and few if any freebies.

Billions of dollars in savings are available simply by leveling out the Medicare Advantage reimbursement process, and indexing MA reimbursement to private market costs rather than Medicare’s insane fraud ridden results.

I meant to reference this paragraph in John’s column: ” Politicians don’t just interfere with overall payment rates, Congress actually gets into the weeds and dictates payment rates on a county by county basis. The reason: to protect vested interests in the districts members of Congress represent. “

Thank you very much for your comment. I agree with your observations about Florida, but I think my proposal is a better solution than yours.

To benchmark MA rates to private plans means adjusting for age which can be done but not perfectly and would also be subject to political interference.

My proposal assumes (hopefully with justification) that MA plans are better at reducing fraud than CMS is. Therefore, under my proposal, the MA rates in Miami and Palm Beach would be about the same. People in Miami who wanted to stay on traditional Medicare Part A and B would have to pay CMS the difference, which would be significant given the figures you cite.

Fraudsters would lose interest and beneficiaries would flock to the MA plans. Fraud would wither very quickly under my proposal. (The speed of the withering would depend on whether the benchmark was the lowest bid, second lowest bid, average, or whatever.)

John, the problem with using Medicare’s county benchmarks is that they are polluted by the fraud that they cannot control. Again taking the case of Miami, Medicare uses probably about $1,400 monthly per beneficiary, and the companies all bid in the range of $1,500, not because it costs that to provide a decent level of Medicare Advantage service, but that it costs that much to provide what is essentially free healthcare for any Medicare beneficiary that wants it in Miami. When the typical Miamian is paying $0 copay for unlimited hospitalization, and the typical resident of Rochester is paying $250/day for 8 to 10 days for the same hospitalization, something is seriously skewed. Benchmarking off minimum or average bid per county will not fix that.

The savings that I alluded to are not from a solution to fraud. Fraud will continue in Miami whether we fix the plan reimbursement process or not. The solutions to fraud are much more complex, and there is probably no political will to make it happen.

I am still not making myself clear. Currently, MA plans compete against each other, but not traditional Medicare. So, the traditional Medicare cost structure forms an artificial floor below which the MA plan has no incentive to compete.

The beneficiary sees none of the costs that we are describing here. The Ryan Medicare reform (which did not exist when I wrote my proposal) would address that problem (although he did not have enough detail on how to adjust the “voucher” for geographic variation of cost.)

[Of course, I would go for Ryan’s plan over my proposal but if Ryan’s plan is a bridge too far, then I continue to hold that mine would be a big step forward.]

To your point: If MA plans knew that if they outbid traditional Medicare A and B, beneficiaries would have to pay more out of pocket to stay in traditional Medicare, the MA plans would also know that those beneficiaries would be more likely to switch to MA than they are now.

So, the MA plans would have an incentive to outbid traditional Medicare which they currently do not. The result would a a virtuous feedback loop with premiums dropping and more seniors going to MA plans.

John and Friends:

As a former satisfied member of a Medicare Advantage plan, I am definitely put out by its closure in San Francisco, with no replacement.

But I am more put out by the completely wrong allegations that Medicare Advantage is more expensive than regular Medicare. There are definitely more services, including reminders to order meds, so the value is greater.

The projections about future costs tend to see trend lines as coming off past experience, without reflecting factors that would bend the trend. In this case, there are three: Medicare enrollees include a rising percentage of people living past the average life span–with continuing costs, but effective medical care that nevertheless can be expensive from “co-morbidities.. And, there are more seniors coming into Medicare than trends would reflect: A pure increase of 4% a year from Boomers, for 20 years. That alone will raise the total cost of medical care. Without provision for this increase, the effect will be waiting lists and deterioration of care intensity, or tertiary care. The third reason is the increase in operating costs from the effects of Obamacare on both contracting health plans and providers. “Staying whole” should mean an increase of about 8% per year, (wet finger.)

As to hospital closures–the AHA reports negative revenue from patient care since 1991. One of the huge reasons is underpayment by Medicaid and Medicare. Hospitals make it up on higher charges to private health plans. If Medicare reimbursement dips below Medicaid rates, you will see hospital closures so numerous that the remainder will be more monopolistic in their service areas and thus able to command higher prices in normal commerce.

Since this is not normal, having the survivors absorb the Medicaid patients thus cut adrift will put them more at risk of closure. First, rural hospitals under 50 beds. Second, inner city hospitals under 100 beds. Third, the smallest and oldest hospitals in a multi-hospital system. Fourth, county hospitals. Fifth, urban hospitals where there is enough remaining capacity to absorb the demand sufficiently that patients do not have to travel backwards to suburban hospitals. Some closures will be triggered by inability to borrow capital to replace an aging facility. As a wave of hospitals were built in the period after WWII, then replaced in a wave during the Seventies, many are well on their way to replacement decisions.

Healthcare is a consumer good as well as being a healthcare good. It is thus mis-leading to set policy of a total expenditure relative to GDP. Note that older people spend money on themselves at an unprecedented rate to look younger, beginning in mid-life. This is also not part of a trend line more than 20 years back. Eyes, foreheads, etc.

I agree with comments about fraud; This is both systemic and regional. It requires a fundamental change in how Medicare processes bills via its fiscal intermediaries. Many are using old software that does not have automatic tests to determine if a spate of bills reflects fraud. As usual, providers are blamed.

A also agree with John about the effect of Health Savings Accounts. We all are seeing the distortions caused by the PPACA; Are we all seeing the risks coming up of some state trying to correct what they see as bad payment policies by instituting rate commissions and nagging Medicare and Medicaid to pay the same rates?

Are we all seeing that further implementation of Obamacare will distort healthcare so much that remedies will be hard to come by?

Wanda J. Jones, President

New Century Healthcare Institute

San Francisco

Wanda:

You got more benefits in MA Medicare, and someone else laid for them — the general taxpayer (now or in the future) and seniors who. Stayed in traditional.Medicare but had to lay higher Part B premiums to help pay for the extra benefits you got.

Now, that you are vexed over losing this benefits, financed by someone else, is a perfectly normal, human reaction. We all like free lunches.

Best,

Uwe

I meant oaid for them. Writing this in a car.

Closer, but still not there. I means paid.

I have stiffened my spine and will (courteously) challenge my friend and mentor, Wanda Jones, on two points.

MA plans offer more value but that does not mean they don’t cost more. They cost the taxpayer more. Should taxpayers fully subsidize all medical care for seniors until the point of zero marginal return? That is unlikely under any system.

With respect to hospitals: Are we so sure we are at the optimal number of hospitals? I’m not. There may be too many hospital beds. I’m also losing confidence in the notion that the hospitals lose money, at the margin, on Medicaid and Medicare.

We read articles concluding this all the time. (I’ve written some myself.) Yet who is the first to lobby to expand Medicaid? The hospitals! I have not seen one hospital jump on to the idea of giving Medicaid patients a voucher to buy private insurance. I am forced to conclude that hospitals profit from Medicaid.

There are some decent issues with MA. One of the top line issues that I see that fuels their popularity is that is their similarity to the employer health care plans.. Just a fixed co-pay etc. Another is the free stuff that they give away to seniors to keep them hooked. United HealthCare had a book where MA recipients could pick OTC medical items ( up to $1,000 per year) and have them shipped to them for free. Who pays for that? Humana offers free gym memberships.Who pays for that? Also, if you think that the formularies are a cake walk, Think again. However, they are better than the ACA plans are at this time especially in the area of specialty drugs. For example, Tier 5 HIV meds have a 33% copay in most MA plans with a max OOP in the Part D scheme. In the ACA world, many of those drugs are NOT on the formulary at all plus the copays are now running 50%. When you are talking drugs that have a $1,500 per month price tag , its unbearable. Co-pay assistance cards usually can’t be used for MA plans which make it even worse. Bottom line: It is more than services that are driving this train.

There are some issues with MA. One of the top line issues that I see that fuels their popularity is that is their similarity to the employer health care plans.. Just a fixed co-pay etc. Another is the free stuff that they give away to seniors to keep them hooked. United HealthCare had a book where MA recipients could pick OTC medical items ( up to $1,000 per year) and have them shipped to them for free. Who pays for that? Humana offers free gym memberships.Who pays for that? Also, if you think that the formularies are a cake walk, Think again. However, they are better than the ACA plans are at this time especially in the area of specialty drugs. For example, Tier 5 HIV meds have a 33% copay in most MA plans with a max OOP in the Part D scheme. In the ACA world, many of those drugs are NOT on the formulary at all plus the copays are now running 50%. When you are talking drugs that have a $1,500 per month price tag , its unbearable. Co-pay assistance cards usually can’t be used for MA plans which make it even worse. Bottom line: It is more than services that are driving this train.

Thank you for your comment. I think you have introduced a good question for research. (It may already have been done): To compare the formularies, co-pays, etc. for Part D plans versus Obamacare plans in the same region.

The treatment of the HIV plans you discuss suggests that adverse selection is worse in Obamacare plans than Medicare Advantage.

You could certainly do such a study. It would show that the political clout of America’s elderly exceeds that of America’s uninsured.

As Medpac and research by others had shown, prior to 2003, when MA plans were paid county-based AACPCs, there was a lot of cherry picking by MA plans (then called Medicare Plus Choice plans). Medicare then used risk-adjusted payments to the MA plans.

But, as is well know, as a result of the MMA 03, MA plans were paid considerably more (on average 14% more) than beneficiaries choosing MA plans would have cost taxpayers under traditional FFS Medicare. Those extra payments allowed the MA plans to offer beneficiaries enhanced benefits — in fact, they had to do that.

That said, it is not clear to me what a comparison of mA plans with OvamaCare plans on the exchanges would tell you. They serve different constituencies with different political clout.

Absolutely.

http://www.treatmentactiongroup.org/copay-letter explains part of the issue about co-pays and co-pay assistance in the ACA world.

I had looked at some MA plans vs. Ohio ACA plans and the formulary differences are very stark. I also believe that because that MA and Part D plans have a big CMS backstop for payment contributes to the issue.

In the ACA world, they only partially subsidize the premium .Please correct me if I am wrong but isn’t the majority of the funding by the Feds for the prescription drug costs in Part D/MA?

I haven’t found such a study yet. I truly believe if a study was done on the differences between the two types, one would find real differences and would further support Uwe’s “political clout “statement.

I work with HIV positive health care consumers everyday in both the MA and ACA world. There are striking differences.

You are right. For Medicare Part D, one eighth of funding is from premiums and seven eighths from government.

The latest Trustees’ Report was released on May 31, 2013. In 2012, premiums were $8.3 billion and total revenue was $66.9 billion, of which most was federal general revenue (see p. 105).

Look at the complexity and, frankly, idiocy of this discussion, and Obamacare has hardly started. This whole thing is a farce. Each government intervention makes an unanticipated mess which then is addressed by another intervention that makes another mess, etc. Isn’t the simplest solution for the government just to get out of the health care market altogether?

I have yet to see a cogent response to my standing observation that, aside from communicable diseases, there is no demonstrated market failure of any significance in health care. That means that, aside from communicable diseases, there is no bases for any government intervention in the health care market WHATSOEVER. There may be a legitimate case to be made for vouchers for poor people, but that is targeted income redistribution, not intervention in the health care market itself.

The market failures in the health care market apparently pale by comparison with those deriving from government intervention.

Doesn’t the current ever-expanding and ever deepening mess at least make one think the foregoing may be reasonable?

And when you establish your one-man, sovereign nation on an abandoned oil rig somewhere in extra-territorial waters, I look forward to your allowing a government-free market for health care.

Meanwhile, those of us who live in the U.S., or Canada, or Great Britain, or Japan, or Finland, or [insert your country’s name here] have to do the hard work of estimating what can be done to limit the damage of government overreach.

There is not one democracy in the world where the demos has not demanded significant government intervention in health care. In the countries that democratized in the 19th and early 20th centuries, it happened in the third-quarter of the 20th century. In the countries that democratized in the second half of the 20th century, it happened within about a decade of democratization (e.g. Taiwan, South Korea).

It even happens in countries where there is growing wealth through commerce without democracy (China, Arab states), so it may be a feature of a certain stage of economic growth, rather than democracy.

Nevertheless, talk of a government-free market for health care is a futile exercise. (We can say the same about government-free markets for education or housing or banking, but that is another post for another blog, I’m sure.)

The reason no one politician is concerned about the future scheduled cuts to Medicare reimbursements is that like the previous legislative cuts to providers they will never happen. (E.g. The doctor fix). The purpose of the ACA cuts to MedicAre was to pass the ACA with a CBO s ore of under $1Trillion. The cuts will NEVER occur as future politicians will override the cuts to stay elected. Obama knew that all along and so do you, John. Uwe, Rick Foster, et al. The disaster will co e but it will be in increased federal budgets far greater than current projections.

Singapore?