How Are Medical Costs Distributed Among the Privately Insured?

Here are some numbers from a 2011 Milliman report on high cost medical conditions in employer health benefit plans in 2010 that might provide a useful frame of reference next time a twenty-year-old claims that high health care costs can be cured by diet and exercise. Keep in mind that these are claims costs for insured patients. The costs might be lower if people were paying cash.

In a typical commercially insured population, only 0.2 percent of people incur annual medical claims over $100,000. Examples of high-cost “routine” events are cardiac revascularization at about $72,000 per year, stroke at $61,000 per year, and cancer patients not receiving chemotherapy or cancer surgery at $14,000 per year.

These events are rare enough that the average claims cost for the total population is slightly less than $4,000.

High cost or catastrophic conditions, the kind that employers purchase stop-loss coverage for, include stroke, cardiovascular surgery, hemophilia, HIV, transplants, end-stage renal disease, newborns with extreme problems, cancer, and people with respiratory failure on ventilators. Of those with catastrophic conditions, about 6 percent of people with these conditions have claims over $100,000. Most fall into the $20,000 to $50,000 range.

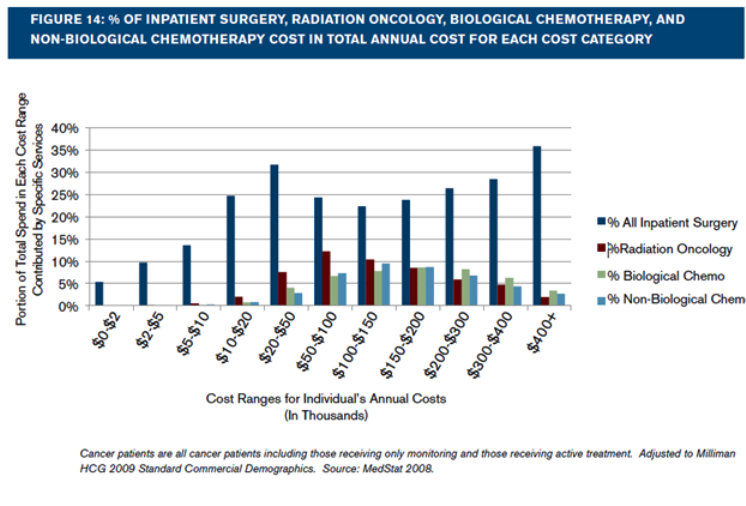

The following graph shows how the costs for cancer patients are distributed.

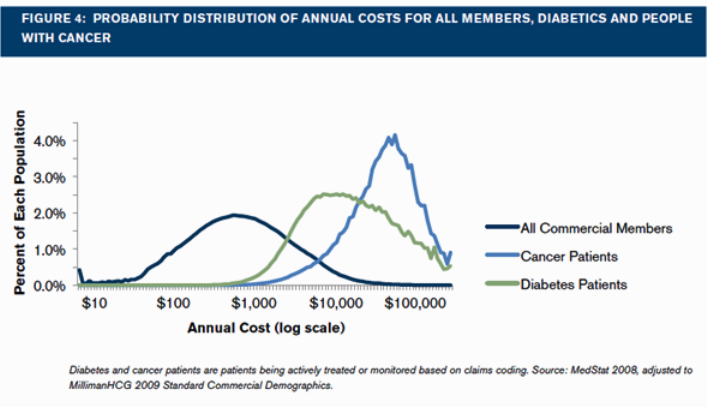

The final graph shows the cost distribution for three populations. The dark blue line shows results for the total commercial population, the green line shows the cost distribution for diabetics, and light blue shows the cost distribution for cancer patients. Note that the horizontal axis is a log scale.

Thanks for the post Linda!

“The costs might be lower if people were paying cash.”

They almost always are.

I haven’t encountered a time when they weren’t, outside of a shopping mall.

“These events are rare enough that the average claims cost for the total population is slightly less than $4,000.”

Impressive. Most impressive.

Thanks Darth Jackson.

“Of those with catastrophic conditions, about 6 percent of people with these conditions have claims over $100,000. Most fall into the $20,000 to $50,000 range.”

Its interesting to hear about how the claims are actually distributed.

“high health care costs can be cured by diet and exercise”

Now if we can only get people to ACTUALLY diet and exercise… oh, wait, no.

You’ll have better luck getting people to embrace communism.

Many already have.

Well, if that’s the case you won’t have to worry about diet and exercise in the work camps.

Great post!

Using similar data, I programmed a spreadsheet to show what would happen to an 18-year-old who, instead of participating in health insurance, were to put his monthly premium in an after-tax healthcare fund for himself, and then self-pay from the fund or by borrowing, if necessary, for any medical expenses.

I employ a random-number generator to randomly hit him with healthcare “incidents” of varying seriousness throughout his life. I can repeat the calculation to get varying results for different “lives.”

Very rarely, when hit with an extremely rare but expensive health “incident,” such as heart transplant, his funds may never be sufficient. But in the vast majority of cases, he will reach retirement well in the black, and in a very high percentage of cases, he will emerge a multimillionaire.

Of course, the fact that a childfree person will never have to deal with the $1M bill for a sick neonate skews the results even further in favor of never carrying health insurance.

No amount of insurance will be sufficient to pay for overcoming death, which is not as rare as the chance of suffering a super-expensive health incident, further skewing the results in favor of never carrying health insurance.

The fact that Obamacare taxes the young, single and healthy male to support the breeding, hypochondriac female and old folks further skews the results against his ever participating in health insurance. Arguing that he will be old and sick someday, too, does not hold up, considering that he may die young or get smart and emigrate in middle age, after having deprived himself, through Obamacare premiums, of fast cars in his youth. On the other hand, any funds he has in a private medical savings account will be available to him at retirement or in better country and can be passed to his heirs if he dies early. Anything his foolish young friends have put into Obamacare will be worth nothing at emigration or sudden early death, of course.

I believe insurance to be nothing more than an exercise in superstition or religion, based on fear and ignorance of simple statistics and probability. I myself will never participate.

Christians other than Amish and Mennonites, who don’t insure, are especially dumb to insure, considering that Jesus famously recommended, “Take no thought for tomorrow … consider the birds of the air ….”

Actually the Amish do insure in their own way. They have a communal bank account for health care expenses, and when one of their members is hospitalized they bring along a cashier’s check for the Medicaid-level fee. And most hospitals accept that.

This is a valuable post. I have done similar research myself into Medicare claims. A tiny percentage of patients pulls up the cost of insurance for everyone else. It is not their fault, of course, but the fault of fee schedules that allow $200,000+ payments.

If paying cash was common, these $200,000 claims would largely disappear. No ordinary person could afford them.

In a lot of cases, hospitals and drug companies would suddenly find that they could treat cancer and premature babies for $30,000. There is a lot of “financial healing” for hospitals when they file enormous claims.

This would however require price controls on expensive drugs with no substitutes. That is one part of health care cost control that conservatives tend to come up short on.

“These events are rare enough that the average claims cost for the total population is slightly less than $4,000.”

Great article, Linda.

I only had a chance to glance at the full report.

“claims costs for insured patients” If this is the “total population” do you know how many lives and the total cost?

I wonder if a comparison of international costs has ever been performed on the catastrophic populations, ESRD, Cancer and neonates especially in relationship to GDP. Alternatively a cost comparison without these three catastrophic conditions?

The Whitepaper on the dataset for 2008 says 24 million covered lives, so presumably the number used in the Milliman report (it used 2008 data) was somewhat larger. Milliman says that it trended the data for cost and demographic shifts in 2009 and 2010.

I don’t know the total cost. It’s not an easy question. One would have to specify the time period, and what constitutes an episode of care. Also, total incurred cost over a year or total paid cost over a year? What about over a person’s lifetime?

Excellent post. I suppose that if we looked at incomes of physicians by specialty it would correlate with this. That is, the highest earning specialties would be treating the most expensively ill patients.

So, if the government were to equalize the incomes of oncologists to primary-care practitioners for example, the consequences would be very bad. (Not that the government proposes to go this far. Nevertheless, much of the talk about increasing incentives for prevention actually means compressing this income differential.)

We’d end up with a lot of healthy people seeing PCPs and a lot of cancer patients unable to get treatment, I suppose.

This post also emphasizes how aburd it is to process almost all medical spending through insurers, instead of paying directly. The average claims per patient of $4,000 suggests a median of a few hundred dollars.

Patients should be able to pay directly for medical care for nine years out of ten without even dealing with their health insurers, like with our car or home insurers.

Thanks John.

Your last paragraph encapsulates my own drumbeat on health reform for the last 5 years.

We need a combination of universal catastrophic insurance for the equivalent of getting hit by a bus, plus price transparency and consumer protection and (in some cases) anti-price gouging laws for the majority of medical care which is ambulatory and to some extent discretionary.

Avik Roy endorsed this odd-but-effective combination of socialism and capitalism in one of his Forbes pieces last year.

There still would need to be some sweating on the details. You need to be able to tax those persons who do not purchase catastrophic insurance on their own. If we are going to have a good emergency care network in the USA, everyone must pay for it no different than fire or police.

And at the other end, you need some kind of control over the hospitals who if left alone will charge someone $1,000 per stitch if they can get away with it. That is the kind of care that should be paid out of pocket, but it is understandable that people want insurance to protect them.

Bob Hertz,The Health Care Crusade

I am not a market absolutist and I appreciate that people coming into ERs after a car accident with a drunk driver are not able to act as effective consumers.

However, that is a small part of medical spending. The ERs are full of people who are walking and talking and could be treated by a primary-care doc or urgent-care clinic if there was one open and available.

As Elisabeth Rosenthal identified in the New York Times (12/2/13), hospitals treat ER’s as profit centers. I think that is where you found your datum of charging $1,000 for a stitch!

There is a lot of hysteria around that $1,000 per stitch charge, but one has to be very foolish to want to create policy based upon that charge of $1,000. Policy really ought to be based upon how much is actually paid per stitch. Hysteria is the left’s answer to policy debate.

Allen, you are correct that hospital charges are wildly in excess of hospital payments, in almost all circumstances.

However, my point was this:

the average citizen is terrified of hospital charges. Unless they feel that these charges are controlled by someone, there will be an equal terror of high deductible policies.

Being terrified might not be all that bad. Terror incentivizes people to learn about what terrifies them. At that point they will find out that they have to look out for #1 themselves and the vast majority will be better off. The hospital won’t be charging $1,000 for a stitch. They won’t even be charging $100 because they will know their patients are empowered and that will level the playing field along with the prices.

But, the truth is that this argument that they might be terrified is hysteria. Likely the vast majority will handle what they are faced without great difficulty much like they handle much more difficult things in their lives.

Allan, I like your spirit but I kind of doubt you have spent much time in hospitals.

I have. The vast majority of patients have no control over what is done to them — which makes sense medically — and no control over what they are charged.

Hospitals are like fire departments, virtually no one is there by choice.

That is why I am a rabid socialist when it comes to hospital care, and a capitalist about everything else in health care. Avik Roy is the same, incidentally, and he is no one’s liberal.

“I kind of doubt you have spent much time in hospitals.”

Strange you say that since most of my life was spent in a hospital or my medical office. I’m a physician that treated a very ill population, but have experience elsewhere as well.

You should understand that no one wishes to be in the position that they need to be hospitalized, but everyone competent that is hospitalized chose to be there.

I believe you to be totally wrong about a patient’s capability in dealing with their own healthcare. However, that ability has tremendous variation and that variation requires different methods of management, not just one, the socialist shoe fits all bureaucracy. It is time to listen and not dictate. Competition is the key so let every modality compete on a level playing field. Choice provides the best option for the most people.

Al, I respect your experience which is more than mine…..and I think you have some valuable insights.

Still I believe that at least one half of all hospital admissions are not elective.

Strokes, heart attacks, CHF, COPD, renal failure, late stage cancer, accidents and violence, drug reactions, it is quite a long list. I do not know how you can say that these patients chose to be where they are.

Second, going back one post, you imply that hospital patients are empowered financially. That baffles me. Unlike the prospective buyer of a new car, they cannot walk away from the deal or try another model.

Nor can they negotiate the bill. The number of court cases where a patient has successfully challenged a hospital can I think be counted on the fingers of one hand.

If you can explain more, I am listening! Best wishes.

Bob Hertz writes: “Still I believe that at least one half of all hospital admissions are not elective.”

Emergency hospitalization is quite a low percentage of total medical expenditures.

“I do not know how you can say that these patients chose to be where they are.”

Because forcefully admitting people to a hospital is a battery. I am sure those entering the hospital didn’t want their illness or broken bones, but the choice of hospitalization is theirs as long as they are deemed competent.

“you imply that hospital patients are empowered financially.”

Actually, I implied that patients, both the well and sick, are empowered. You don’t suddenly end up in a restaurant that serves lousy food at $200 a plate. You prepare for it and choose the best restaurant that fits your needs. Same with medical care. Of course you might be out on the road in the middle of nowhere where you need to eat and you have to go into the only available restaurant and pay extra. At times that happens. Same with medical care. You can be in a desert dying of thirst and make a contract for a bottle of water for $1Million but that contract will not be upheld in court. Same in health care. You might end up being charged more than usual which is the same in both instances except in health care the hospital must provide the emergency/urgent care even if it is known in advance that the patient won’t pay.

“Nor can they negotiate the bill.”

That is absolutely untrue. Negotiations occur all the time. That is one of the reasons hospitals have so many people working in the billing department that have the ability to negotiate on the hospital’s behalf. (Please note that I am not saying that hospitals always act appropriately. They don’t!)