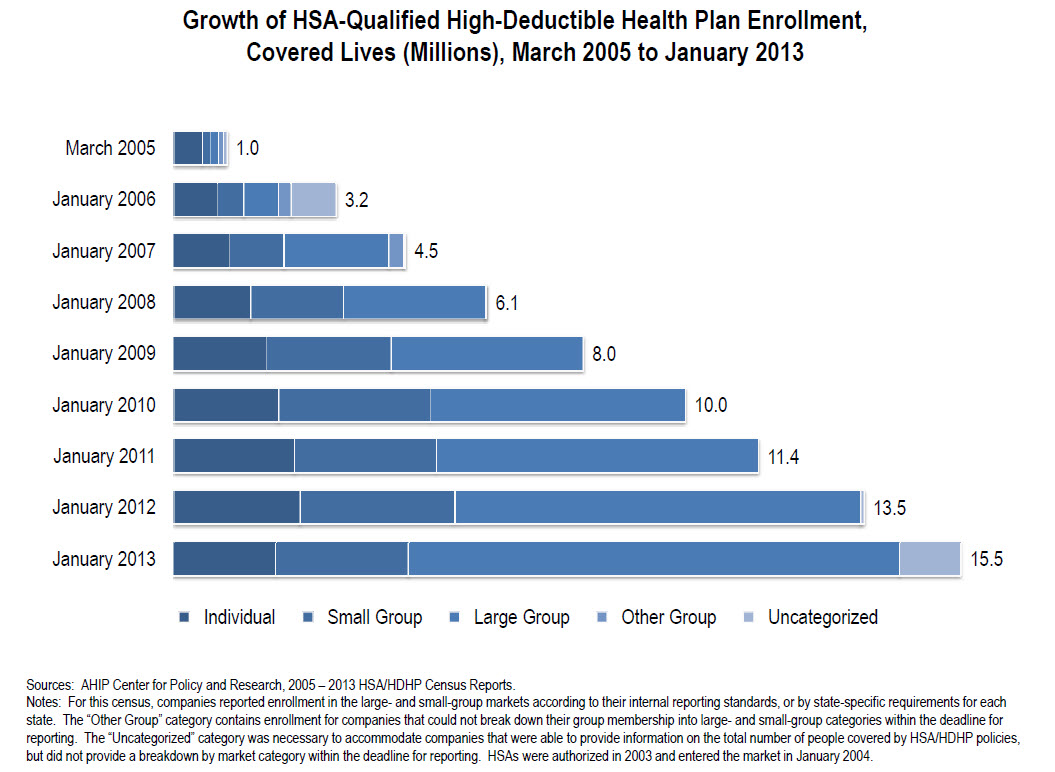

A Brief History of Health Savings Accounts

Devon Herrick, a senior fellow at the National Center for Policy Analysis (NCPA), writes:

- I

n January 1984, the NCPA published a plan to use individually-owned “medical IRAs” to solve the long-term problem of Medicare.

n January 1984, the NCPA published a plan to use individually-owned “medical IRAs” to solve the long-term problem of Medicare. - Two months later, NCPA President John Goodman and Richard Rahn, then chief economist for the U.S. Chamber of Commerce, outlined this plan in a Wall Street Journal article.

- That same year Singapore introduced a mandatory “Medisave” program.

Goodman and Senior Fellow Gerald Musgrave wrote a seminal study documenting opportunities in the United States to select high-deductible health insurance and place the premium savings in a personal health account to pay for small medical expenses.

In 1990, the NCPA organized a taskforce of researchers from 40 think tanks, universities and research organizations, including the American Enterprise Institute, the Cato Institute and the Hoover Institution. The report advocated self-insurance for small medical bills through Medical Savings Accounts (MSAs).

Capitol Hill responded quickly. In 1992, 12 different bills designed to create Medical Savings Accounts received the bipartisan support of 150 congressional cosponsors, including both conservatives and liberals. (More)