PPI: Gap in Hospital Inpatient & Outpatient Prices

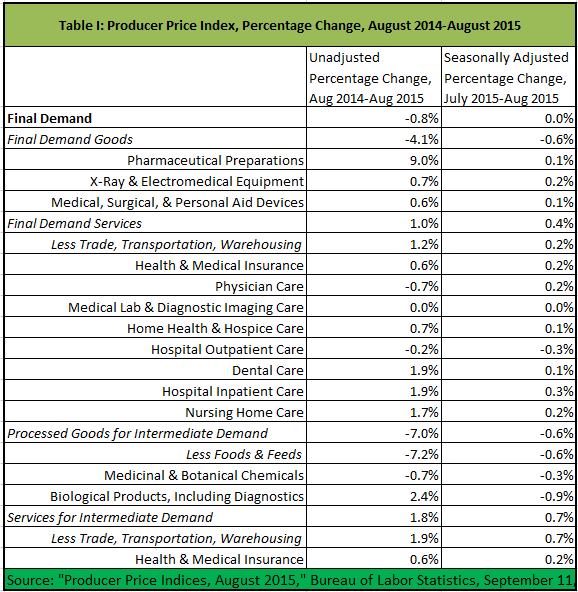

August’s Producer Price Index was flat, month on month, and dropped 0.8 percent, year on year, continuing the trend we saw last month. Producer prices for health goods and services are rising faster than other producer prices (see Table I).

August’s Producer Price Index was flat, month on month, and dropped 0.8 percent, year on year, continuing the trend we saw last month. Producer prices for health goods and services are rising faster than other producer prices (see Table I).

Outside health care, goods for both final and intermediate demand declined from July. Although it has taken a while, it looks like prices increases for pharmaceutical preparations and their inputs are moderating significantly. Prices for medical devices are still growing faster than prices for final demand goods overall, but not dramatically so.

Producer prices for health services actually grew a little slower than prices of other services. What is interesting is the difference in the rate of inflation for hospital inpatient versus outpatient services. Outpatient prices are declining, while inpatient prices are rising, resulting in quite a gap.

I’d like to believe the outpatient prices are under pressure from ambulatory clinics. As for inpatient prices – well, this data gibes well with the Quarterly Services Survey, which showed an increase in hospital profits.

To your knowledge, is there any pressure on hospitals to make their consumer pricing any more transparent? By pressure I mean politicians, lobbyists, consumer groups or progressive activists attacking the issue forcefully and persistently.

It needs more than blogs, columns and magazine articles; it needs passion.

I would say the hospitals understand the problem, but they are not feeling enough pain to do enough about it.