Obamacare Might Have Enrolled Only 2.3 Million; Spent $73 Billion to Save Less than $6 Billion in Uncompensated Care

Things change fast in Obamacare. Just yesterday, I discussed evidence that Obamacare had enrolled only 6 million people in subsidized, private plans on exchanges. Having read the U.S. Department of Health & Human Services’ (HHS’) latest report, it looks like the figure is only 2.3 million: “Based on an estimated 10.3 million decrease in the total number of uninsured and an estimated 8 million increase in the number covered by Medicaid, ASPE estimates that hospital uncompensated care costs will be $5.7 billion lower in 2014 than they otherwise would have been.” The difference between 10.3 million and 8 million is only 2.3 million, and that is quite a comedown from HHS’ May estimate that 8.1 million people “selected” private coverage in exchanges.

If we were asked to give a one-sentence justification for Obamacare’s increased federal spending on Medicaid or tax credits for private health insurance, it would go something like this: “People with health insurance will get timely primary care, and that will relieve the pressure on hospitals’ emergency departments.” This feel-good statement has been rolled out countless of times by advocates of so-called universal coverage. Empirically, it falls flat: Emergency departments are jammed with both Medicaid dependents and (somewhat less so) privately insured patients.

However, it does benefit hospitals, which can monetize more of their ED care, which was previously uncompensated. Let’s accept that $5.7 billion estimated drop in uncompensated care costs. How much did it cost taxpayers to buy that reduction?

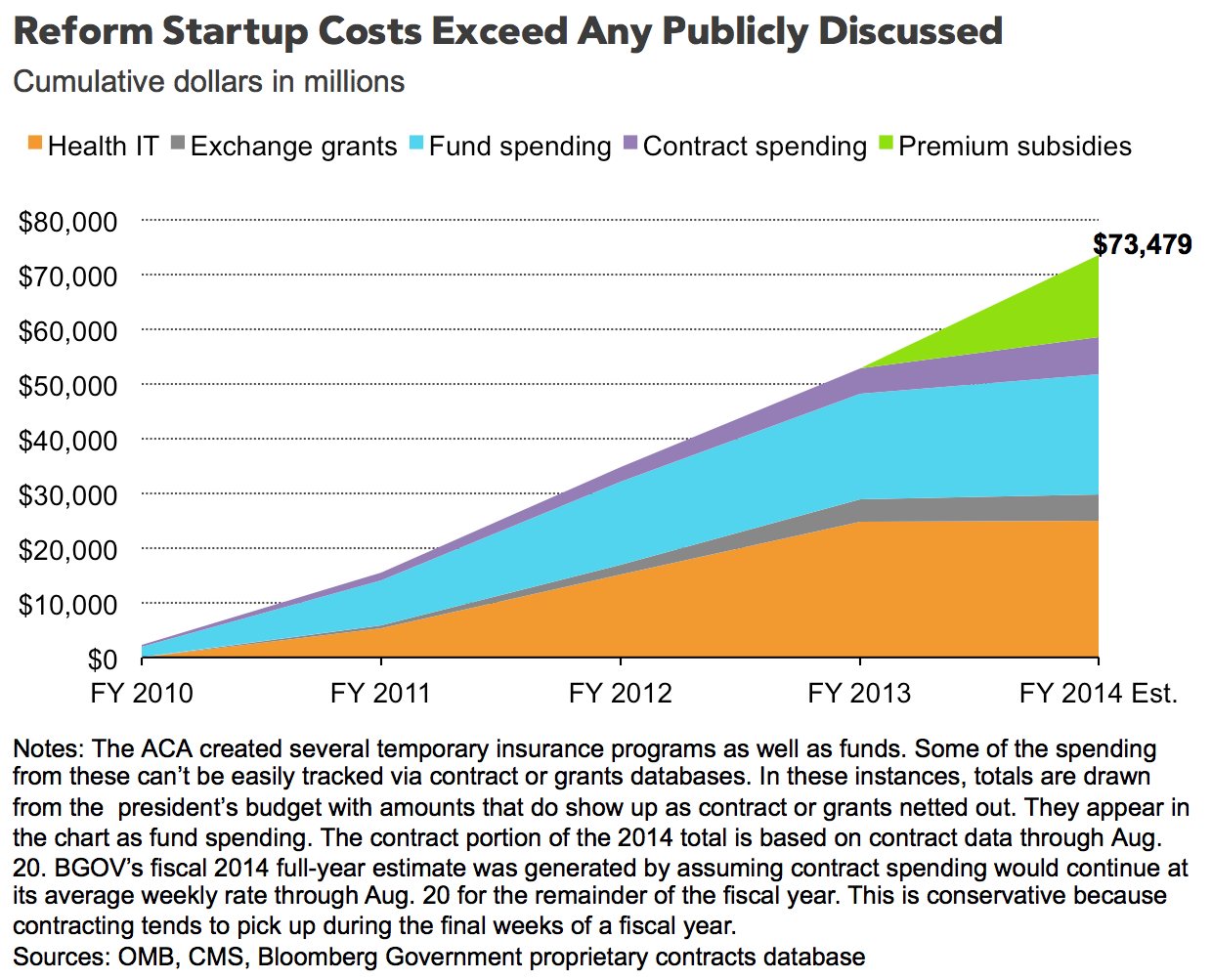

The answer comes from Bloomberg Government’s Peter Gosselin: We’ve spent $73 billion on Obamacare so far. Gosselin has added up all the spending on health IT, grants, contracts, and subsidies, as shown in the chart below.

Spending $73 billion for a return of $5.7 billion. Obamacare is an amazing waste of money.

The leftish arguments about savings on emergency care have always been a big big stretch.

Agreed.

But you miss a point, John. A good chunk of the $73 billion has gone toward subsidies that have lowered the net premium paid by many thousands of indvidual buyers.

These persons are clearly better off. People in their 50’s with modest incomes and no employer coverage are tremendously better off than before the ACA.

I am not saying that these savings (for some) makes the whole ACA a great thing. But you leave it out in this post.

In a democracy (even in a tyranny), it would be absurd to think of a policy that made nobody better off. Nevertheless, if we think the government knows that taking one dollar from X and giving it to Z will make Z better off than it makes X worse off, there is no end to the possible tinkering.

@bob hertz

Prior to the ACA, nearly all of the states had high risk pools for the uninsurable. The first phase of the ACA included a federal high risk pool as well. It would have been far simpler, just as efficacious, and way less expensive to provide subsidies to those in the risk pools who could not afford coverage. Same result, less trouble.

I like what you are saying. But let me raise two cautions:

Before the ACA, 15 states had no risk pools and about 15 more had tiny amounts of funding so there were long waiting lists. These states were not willing to raise any taxes whatsoever for risk pools.

So, it would have taken some federal coercion and federal funding to create the pools that you endorse.

Second point: Some of the beneficiaries of the ACA are not high risk at all. They are just 55 years old have incomes under $30,000 a year. They used to find health insurance unaffordable, and this would happen again in a New York minute without the ACA.

FYI, I sold health policies in the Texas Pool and the Federal pool before they were abolished.

As to your first point, federal subsidies to fund them.

As to your second point, I have never met an insurable 55 year old under the pre-ACA regime. Being 55, for all intents and purposes, made you uninsurable and qualified you for the high risk pool. You were not uninsurable because you were 55, per se, but because, by age 55, for the vast majority of cases; pre-existing conditions and other morbidity factors made you uninsurable. There are few, if any, completely healthy 55 year olds, with no pre-existing conditions or disqualifying morbidity.

Because the federal government cannot get any money other than from the fifty states, any subsidy it gives Texas must be taken away from the other fifty states ( and DC and territories, but I simplify for exposition.)

(Even though the federal government can borrow from the central bank of China and states cannot, U.S. taxpayers have to repay that debt.)

What you say is certainly true but beside the point discussed here. My point is that if tax dollars are spent subsidizing premiums, then the pre-ACA regime, subsidized, would have required many fewer tax dollars than the present regime for the same effect.

I think I agree with you there.

John, your statement about taxes baffles me. Social Security and Medicare taxes are federal in scope, so in no way do such taxes take from Texas and give to Maryland.

If a worker spends six months in each state, his SS taxes are the same.

But we might be going down a rabbit hole in this area.

Jardinero, thanks for your comments. I have wondered myself if what you say is true.

Let’s say we had no ACA at all other than subsidized high risk pools. And say that we allowed insurers to keep denying coverage for pre-ex conditions.

This would mean a large bloc of persons who do not have employer coverage, and would be denied individual insurance.

How big is this bloc?

If this bloc is 10 million persons ( and I think it is more), and we gave each of them enough money to make private insurance affordable, we would be giving each of them about $3000.

This is $30 billion a year and i think my numbers are low.

Is this a whole lot less than the ACA subsidies? I am not so sure.

My personal opinion is that the “bloc”, you refer to is not ten million but likely much less. My reason is thus, the federal pool hit something like a million or two before it closed down. I conjecture that most of those came from states with crappy state pools. I don’t believe there were more than six million in the state pools before they shut down. I don’t know, but I conjecture that many of those in the state and federal risk pools drifted over to the exchanges this year, because of the subsidy offered in the exchanges, but not in the pools. I believe that they are the majority of enrollees in the exchanges. I readily admit that I am making back of the envelope estimates, but they square with the enrollment pattern we saw in the exchanges this year.

Between the pools, clinics and county hospitatls, I have never believed that it was impossible to find coverage or care in this country – Pre ACA. I think affordability was an issue for many – Pre-ACA. The simple solution to affordability is to increase supply, increase competition, increase choice and for the very poorest – provide subsidies. I reluctantly list subsidies for only the very poorest, because subsidies increase demand/prices and affordability.

One more thing. This is difficult for many to fathom but there is a large cohort of uninsured persons who truly do not desire conventional health insurance. I suggest that this accounts for the vast majority of the uninsured. Many refuse because they aren’t sick. Many, actually, are sick or have been sick and prefer to milk the system of clinics and county hospitals without paying. Many are sick and prefer to pay cash or make payments. I have met many who fit in each of these cohorts and they come from all walks of life; independent contractors, consultants, doctors, dentists, lawyers, small business people. They readily choose not to purchase insurance.

WE are going down a rabbit hole. But why not.

Medicaid, Obamacare, and uncompensated care are all “charity care”. To keep the charity care within the community has got to be more efficient than the government forcing every community to cross-subsidize each others’ charity care, with a huge bureaucracy in the middle.

Good comments.

My only disagreement is with the statement that competition will increase affordablity. That may be true for ambulatory care such as office visits and diagnostic tests.

But I do not know any way to make brain surgery or stage 4 cancer treatment “affordable” out of pocket. Some form of insurance will always be needed.

My own solution would be use Medicare as the payer of last resort for end of life cases. Saves a ton of bureaucracy and regulation of insurers, and probably would cost $30-$50 billion — no more than the subsidies we will pay now.

You have an interesting idea about end of life cases. My wife is an operating room nurse and there are many continuous innovations going on which make surgeries both cheaper and more efficacious. The biggest innovations are actually in robotics. Open cases which required three days to a week for recovery are now day surgeries because of robotics. An example of such is here: http://www.davincisurgery.com/

There is insurance in all markets, but insurers do not fix prices of the goods they indemnify. That is the difference.

John, you raise an interesting point about charity care in the community.

Back in the 1950’s, you had a higher percentage of county hospitals, and you had local medical societies which could informally ask doctors to assist in charity cases.

This would be damned hard to reconstitute in today’s world of for-profit hospitals, greedy non-profit hospitals, doctors in many different corporate structures, et al.

Plus there is the old liberal fear (and not totally unwarranted) that states like Minnesota and New York would offer far more charity care than Mississippi.

In Medicaid and high-risk pools and subsidized health insurance before the ACA, the variations were enormous.

Some would call that the charming individuality of the states. Others would call that stinginess and racism.

Any program to decentralize charity care would have to meet this objection, at least it would have to meet this objection to satisfy me.

With any system there is always the risk that disparate groups will receive disparate, not necessarily equal, treatment. It is a fallacy to assume that centralizing the payment mechanism, via medicaid or direct subsidy, will insure equal treatment. A dollar spent for care at a county hospital in Mississippi or East Texas is not going to get you the same level of care as a dollar spent at the Mayo Clinic, Texas Childrens Hospital, or Cedar Sinai Medical Center. No amount of centralized payment can undo regional and institutional differences in care.

Exactly. The central government can dictate the cashflows but it cannot dictate uniform quality or accessibility.

As to Mr. Hertz’ comment: It invites the question of how we got “greedy” non-profit hospitals. They are still run by the same confessional groups that run the soup kitchens, but we do’t have “greedy” soup kitchens. Could the government take-over of health care contributed to the “greed”?

John, there are many many articles about non profit hospitals acting very uncharitably. There is absolutely nothing in common between the Salvation Army and a big hospital, even a hospital run by a church.

Here are just two citations:

http://blogs.marketwatch.com/thetell/2013/02/21/nonprofit-hospitals-pay-leaders-millions-charge-uninsured-huge-markups-time

http://lawjournal.rutgers.edu/sites/lawjournal.rutgers.edu/files/issues/v42/1/George%20A.%20Nation%20III,%20Non-Profit%20Charitable%20Ta

Yes: We are on the same page. However, if you look back before Medicare and the federal role in hospital insurance, I think you will find that hospitals behaved much more the way they ought to behave: Relying on the community for support.

I assert that the government take-over of health care has perverted hospitals’ incentives and mission.