Louisiana Shows Coverage Does Not Equal Access

![]() Readers know I disagree with using measurements of “coverage” as proxies for access to medical care. New data from the Louisiana Department of Health, which cheers the expansion of Medicaid dependency in the state, shows (unwittingly) exactly why.

Readers know I disagree with using measurements of “coverage” as proxies for access to medical care. New data from the Louisiana Department of Health, which cheers the expansion of Medicaid dependency in the state, shows (unwittingly) exactly why.

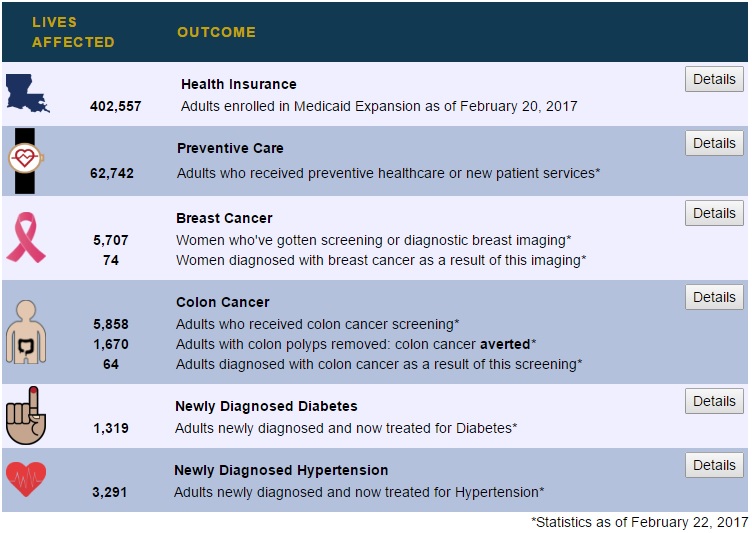

Healthy Louisiana’s Dashboard shows 402,557 adults became dependent on Medicaid as a result of Obamacare’s expansion. The Department notes benefits for some sick people. For example, screening resulted in 74 people being diagnosed with breast cancer and 64 diagnosed with colon cancer.

The Dashboard stops there, not telling us how those newly diagnosed were treated. (Medicaid patients often receive treatment later than privately insured.) However, there is another, likely bigger problem.

Of these almost half million newly dependent, only 62,742 received “preventive healthcare or new patient services.” As David Anderson of the Duke-Margolis explained to me on Twitter, this excludes those who became dependent on Medicaid who were already being treated or did not get any treatment. That is, the Medicaid enrollment resulted in zero change in access to health care for 339,815 of the newly dependent. That amounts to 84 percent of the population.

Why did these people enroll in Medicaid when they were already receiving care or did not want to receive care? Well, the Medicaid expansion involved a lot of promotion, including enrollment “fairs” in high-traffic areas, so why not sign up and get a balloon or lapel pin or whatever?

More seriously: Those receiving care either paid for it or received it as charity. If they paid for it themselves, we need better understanding of whether this drove them into financial distress or not. If they received charity care, taxpayer funding is unnecessary. (Indeed, if taxpayers are funding Medicaid to pay for care doctors and hospitals would give anyway, the Medicaid spending is simply a transfer of consumer surplus from taxpayers to doctors and hospitals and likely imposes a deadweight loss to society because it reduces taxpayers’ incentive to work.)

Of course most of the privately insured population is healthy at any given time. However, they are paying for “insurance” and cannot just get it whenever they want. People who get Medicaid do not need to enroll in open season: They can sign up when they get sick.

So, measuring health reform’s success by the number of people covered by Medicaid expansion is a very, very poor way to estimate increased access to health care.

The most revealing statistic for the accessibility of healthcare in each State is probably the State’s maternal mortality ratio. The data sets for this measure are hard to find, since the data has not been available since 2007. The only meaningful data sets that have existed, state by state, are for 1986-1992 and 2001-2006. Among the 50 States, Louisiana ranked 43rd in the first data set and 42nd in the second data set. Coincidentally, the State of New York ranked 49th in the first data set and 46th in the second. Yes, the rankings are from best to worst.

.

A new analysis of our nation’s maternal mortality ratio data appeared in the September 2016 edition of the Obstetrics & Gynecology journal. It also explains why the state by state data has not been available since 2007. Unfortunately, our nation’s maternal mortality ratio continues to worsen: 20.3 in 2004, 22.0 in 2009, and 23.8 in 2014 (as it has for 30 years). By comparison, the 10 developed nations (out of 48) have maternal morality ratios that average 3-4 deaths per 100,000 live births annually. The awareness of this issue, state by state, is well recognized but not widely acknowledged. By far, it is the most widely applicable attribute of our nation’s healthcare problems that requires an immediate long-term solution. The intense “fog” surrounding healthcare reform largely ignores the needs of each individual citizen, community by community. The fog has institutionally paralyzed many efforts to energize the community by community voluntarism for its own COMMON GOOD.

.

The many efforts to improve our nation’s maternal healthcare have been only marginally effective. Six states in 2001-2006 already had a “normal” maternal mortality ratio: Alaska, Indiana, Maine, Massachusetts, Minnesota and Rhode Island (as compared to the other developed nations). My professional opinion is that this problem and the cost of our nation’s healthcare will NOT be solved without a means to also improve the level of SOCIAL CAPITAL that exists, community by community. Universal Health Insurance is important for the equitable availability of healthcare, but insurance coverage has much less to do with its ECOLOGIC accessibility.

You MDs are a one trick pony, except Allan, hez smart. Paul you keep saying over and over, “energize the community by community voluntarism for its own COMMON GOOD.” Sure, sure, you and Hillary say it takes a village but we know it doesn’t require a village to have a plan, get real. Trust me, nobody cares about Obstetrics & Gynecology anymore. That is boring yesterday’s news.

Maybe our maternal mortality rate will improve if Trump is able to limit the amount of illegal drugs coming across our borders.

A very good thought!

A second thought: reduced elicit drug availability might actually be more helpful for New York. The major issue for Louisiana is its level of poverty.

Absolutely. A major problem for most of our outcomes when compared to other nations has more to do with socio economic considerations than the healthcare system. Therefore though we need to dump Obamacare and provide a more marketbased system these other problems will have more of an effect on our healthcare ratings since the statistics being used to rate us have little validity for a rating system of healthcare system quality.

Absolutely right. The “health care system” accounts for between 10 percent and 50 percent of our health status, according to my understanding of the research.

MAGICAL TrumpCare will suck these Medicaid people away in a HUGE way, that’s for sure. MAGICAL TrumpCare is coming and young people WIN BIGLY. Age-based tax credits for the purchase of personal, portable and permanent Individual Medical (IM) insurance and larger tax-free HSAs! I enrolled the USAs 1st tax-free HSA in 1996 so you can trust me. Nobody is going to pay $1,000 a month to add their family to their employer’s insurance when President Trump is giving it away for FREE. Wait it gets better. The CEO of United Health Care will say, “President Trump is paying these people $1,000, TAX FREE, in their tax-free HSA to switch off our employer-based insurance so our stock will drop to ZERO!” Want to be a multi-millionaire? Short these stocks: INVESTORS’ NOTE: The biggest publicly-traded health insurance companies include UnitedHealth (NYSE:UNH), Anthem (NYSE:ANTM), Aetna (NYSE:AET), Molina (NYSE:MOH), and Centene (NYSE:CNC).

Read about it here: LARGER AGE-BASED TAX CREDITS https://www.forbes.com/sites/theapothecary/2017/02/26/leaked-draft-shows-gop-plan-will-not-only-replace-obamacare-but-transform-medicaid/#3b9e939b3cea

So right!

Coverage does not mean health care, but only insurance, the benefits of which are diminished by exclusions, deductibles and co-pays.

And, maybe worst of all, that insurance coverage is not available for the doc of your choice or the hospital of your choice, especially one in Mexico, Cuba or lots of other places that offer Medical Tourism at greatly reduced prices.

If you participate in health insurance of any kind, you are a second-class citizen when it comes to real health care.

not great but its a start. Guess it will take awhile to clean up the mess.

Looks like Employers will just drop plans and contribute to HSA accounts. Tax credits up to $14,000

Up to age 29 gets $2,000 up to 39 gets $2500 up to 49 gets $3,000 up to age 59 gets $3,500 age 60+ gets $4,000

$15 Billion allocated per year for first few years to state high risk pools.

Minimum health benefits determined by states.

removal of all individual penalties and employer mandates.

http://www.politico.com/f/?id=0000015a-70de-d2c6-a7db-78ff707e0000

I saw something there about changing age banding to 5:1 for new policies. Does that mean no underwriting?

That change alone would continue to eliminate health status as a means of underwriting.

Why have High Risk Pools and no underwriting on individual Medical (IM) insurance?

? not sure what you are saying John.

moving the age banding from 3-1 to 5-1 will just allow the young to pay less than the older. we will still have underwriting.

WTFAYTA?

I couldn’t understand the relationship between the $14,000 and the age-adjusted credits of $2000-4000.

Maximum credit per family is $14,000. Young people make out BIGLY.

30-year-old father is $2,500 + 1 child at $2,000 means an annual tax credit of $4,500. Any unused credit goes to the tax-free HSA so just like the MSA days everybody will go with the highest HSA Qualifying deductible for the smallest premium which will create the largest HSA deposit from the Feds. This means those states with the lowest premium will have the largest HSA deposits.

If the $6,550 deductible was the same premium as a $2,500 STM plan then this is an example of premium and HSA deposits. On the family above:

Florida premium $3,120 and HSA deposit of $1,380

IOWA premium $2,040 and HSA deposit of $2,460

New York ? $5,000+ and HSA deposit of $0

Sorry New York and your expensive guaranteed issue

Because I am a sales trainer this is the close we train the insurance agent in the future selling MAGICAL TrumpCare:

Closing Question 1: Will you let President Trump pay for your health insurance with age-based tax credits IF he pays you $2,460 TAX FREE? (wait for a yes or no)

Closing question 2: This is similar to an IQ test isn’t it? (wait for a yes or no)

Closing question 3: Am I going too fast for you? (wait….)

This will be like taking candy from a baby, a blind baby.

John, thanks for a very interesting post on Medicaid.

I am seeing a disconnect between the national statistics (which say that Medicaid is costing $6,000 per beneficiary)

versus these statistics (which show 64,000 preventive care visits at let’s say $200 each, for just $13 million in spending, plus a smattering of cancer diagnoses.) I do not see any hospitalizations in your statistics.

I wonder if it is just too early to measure the cost of Louisiana’s Medicaid. Maybe it takes a couple of years to get some premature infants and heart transplants into the case mix.

I know that in the non-Medicaid ACA exchanges, it sure did not take long for big claims to hit the insurers. Maybe the Medicaid population is healthier?