How Narrow Are the Narrow Networks?

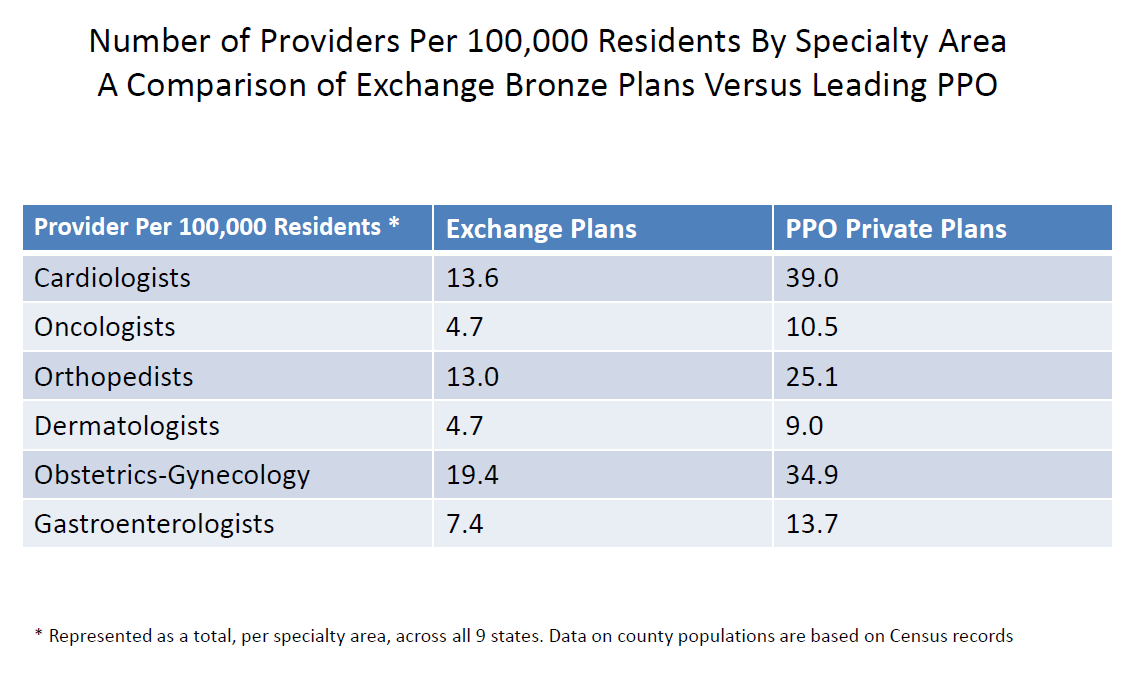

Source: Scott Gottlieb’s testimony before the Committee on Ways and Means Subcommittee on Health, from the AEI.

Source: Scott Gottlieb’s testimony before the Committee on Ways and Means Subcommittee on Health, from the AEI.

That’s a pretty stunning graph.

That sounds like a great business for those few doctors. If they are the only ones that the insurance will cover, that means that they will get more business. I wonder how those doctors were selected. I think that many of those doctors are willing to work for a few years with that insurance and then stop accepting it. Many patients would keep coming even if they had to pay some more.

Once they see how lousy the reimbursement is, believe me, they will pull out of those plans. At some point they will reach diminishing returns.

While its good for the doctors, as the increased demand will be good for business. The patients are the ones who will suffer. Increased wait times, shorter appointments and lack of options hurt the consumer.

No, not good for the doctors. They are already having to spend too much time on needless, nonpertinent documentation and inadequate EMR systems. Many are unhappy about not being able to spend quality time with their patient as is.

It is amazing that exchange plans have nearly half the providers that PPO private plans have. Good luck to anyone who has an exchange plan and needs to see a specialist.

I wonder if the insurance companies have to take the Hippocratic Oath. I believe they should. At the end they are an essential key, with our current system, in providing health care to the people. The well-being of the patient should be placed first, regardless if you are a physician or the insurance company.

But this is also a business in the end as well. While health care should always put patient first, in this new system they need to at least be profitable.

Only a third of cardiology providers compared to PPO. Heart disease is already a leading cause of death in this country, it will make it worse when ObamaCare will limit your options of finding a cardiologist.

A program that sought the well-being of everyone ended up being prejudicial to the majority of Americans. Instead of trying to make a major overhaul to the entire system, why didn’t we tried to help those who couldn’t afford healthcare while keeping the status quo of those who had coverage that satisfied their needs.

Amen!

The million dollar question…

Why tweak the system when you can blow it up? Obama wanted to go down as the one who lead the rebuilding of America. Instead he will just be the one who tore it apart.

He wanted to leave a legacy, and what better than by overhauling the whole system, which affects every American, with a program that carries his name.

The difference in network demonstrates that the government made lots of assumptions when they reformed the health care system, and most of them were wrong. ACA is not a program that benefits the majority of the population; it benefits a few at the expense of the many.

This indicates that the demand for doctors will be increasing.

I have no love for the ACA, but I am not positive that all the blame for narrow networks resides in Washington.

The ACA law had nothing to say about networks, to my knowledge.

The state insurance commissions do not supervise the size of networks, to my knowledge.

Now when the insurance companies designed compliant plans for 2014, they have all come out with narrow networks.

Do we entirely know why?

Is it because in the absence of underwriting, this is a quiet way to keep out unhealthy customers?

Is it because narrow networks are a proven way to stay profitable?

This issue is more subtle than just blaming Obama.

In New York the DOH used HMO networks as template for Exchange plans which narrowed Exchange networks. The DFS had the authority to not follow this in the individual market and to provide alternatives with more expansive networks. It was not obligated to follow the DOH, but apart from Western NYS, individual plans are overwhelmingly HMOs with similar narrow networks. It does not amount to State action anti-trust, because DOH and DFS have the out of periodically reviewing the networks (which they knew from the outset were too narrow and effectively circumvented Obamacare out of network coverage maximums). Not politically likely to see anti-trust lawsuit against Exchange, DFS and DOH, but effectively it is what was permitted and is happening. At the same time ACA precludes Associations and Chambers of Commerce from offering its individual members the broader and cheaper plans they did, and has thrown those members into the deficient and more expensive individual market. Rather than being pro-consumer, ACA is anti-consumer, because individuals buying through a group get better and cheaper coverage. This is evening more perverse in NYS, because it is a community rated state, so individuals would not be individually underwritten and rated in any event. Effectively, the individual middle class (above 400% of FPL) have been forced by Obamacare and Cuomocare into a poor insurance system, that charges them more, forces them to lose doctors (and hospitals) that they have used for decades, and substitutes an a narrow network (often the same in different plans)that will have them self-insure despite paying higher premiums.

The graph is incomplete. There ought to be a column showing the number of docs available to the cash-paying patient who forgoes Obamacare altogether.

I pay cash and enjoy a worldwide network of millions upon millions of docs. I’m having cataract surgery in Rio next month for half the fair price charged in the USSA.

And let us not forget the Colorado health exchange Elevate plan. It has a “network” consisting of exactly one hospital, along with the physicians, clinics, and pharmacy associated with it.

Good comments from Brook White. I was not aware that the New York Insurance commission took such an activist role in pushing insurers to use narrow networks.

Actually there are several aspects of the ACA where the most harmful decisions have actually come from state regulators.

Not that Washington would have done any better.

Bob,

People who buy health insurance in the individual market are extremely price sensitive. Narrow networks generally cost 25%-30% less than broad network PPO’s. If the excluded hospitals and doctors weren’t so determined to use their market power to extract exorbitant prices from insurers for each service, test and procedure it would be more feasible to include them in the network. With medical underwriting now outlawed and the essential benefits package defined in the legislation, narrow networks are the only tool left in the toolkit to keep premiums at least close to reasonable.

The New York individual health insurance market has only a tiny number of participants (pre-ACA) as a percentage of the population because of the combination of community rating guaranteed issue and no mandate to buy insurance. It’s a recipe for classic adverse selection and that’s what they got. Now that there is a mandate to buy insurance, premiums are coming down from ludicrously expensive to merely expensive.