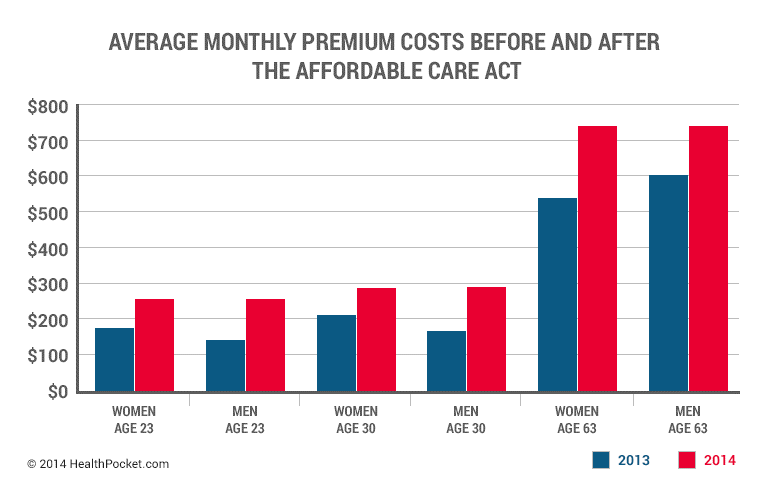

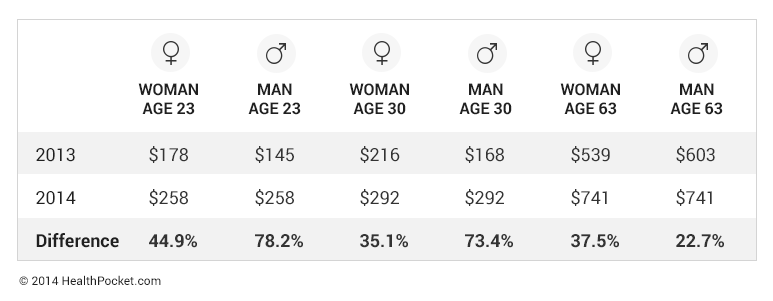

Obamacare Premiums Increased Dramatically for Every Age Group in 2014

HealthPocket, an online insurance broker, has measured the increase in premiums for every age group in Obamacare versus the pre-Obamacare individual market. Their conclusion: Premiums increased by double digits for every age group.

What I find really surprising is the increase in rates for 63-year olds: 37.5 percent for women and 22.7 percent for men. Recall that Obamacare forbids actuarially accurate underwriting by age. The difference in rates between young adults and older ones can be no greater than three to one. We’ve already discussed that this must raise rates for younger people, because actuarial consensus is that average health spending for 63-year olds is five times that of 22-year olds.

Politically, the purpose of squeezing the age bands is obvious: The younger person, who is unlikely to vote, subsidizes the older person, who is much more likely to vote. If this had happened, I expect Obamacare would be more popular than it is today. Now, HealthPocket does point out that these are unsubsidized premiums: Obamacare disguises these true premiums by offering health insurers tax credits to reduce the net premium people pay, thus fooling many into thinking that premiums have gone down.

Another issue to point out is the difference in changes for men versus women. Obamacare’s supporters made a big show about outlawing “discrimination” against women, and forcing insurers to charge the same rate for both sexes. Premiums for women of child-bearing age had been higher primarily because of the costs of childbirth. However, this turns around after child-bearing age: Men have higher costs. So, Obamacare caused a higher increase in premiums for older women than older men.

The old people are subsidizing the young with contraceptives and 26 year olds being on their parents plan. All those extra bells and whistles cost money, I am not surprised by the across the board increase.

These premium increases are substantial

The media will probably focus on the net not the gross premium

Does any one have figures on how much of these gross increases are covered by subsidies

I would guess 70 percent which would be substantially higher than the employer tax exemption on a percentage basis

In addition I believe such high subsidies naturally increase the premiums faster than with lower percentage subsidies

Don Levit

Managing .Partner

National Prosperity Life and Health

Seven hundred a month? Perhaps HealthPocket should consider changing their name to HealthCheckbook.

The fact of the matter is that even subsidized premiums result in an out of pocket premium that is guaranteed to be eight percent of your AGI. Many persons, especially the young and healthy, did not pay eight percent of their income in premium under the old regime. Many persons, also had policies with extremely low deductibles under the old regime. Now everyone pays eight percent of their income and a two thousand dollar deductible, minimum. So now, if you are never sick you pay a much higher premium, even if you are subsidized. If you are sick, the you are now likely paying more out of pocket.

That’s what happens when political egalitarianism forces itself upon capitalistic insurance actuaries. Indeed, quite the conundrum for the handsome young Indonesian actor, Barry Sotero, who plays the president of the United States on TV.

Higher government “subsidies” just means ACA ends up costing even more.

Taxpayers still foot the bill for the whole cost.

People who aren’t paying much tax won’t notice and anyway have no reason to care.

How to help the middle class – 2014 edition.

Before the ACA, in states that allowed full underwriting, the premium ratio of old to young was about 6 to 1.

The young person paid $150 per month, the old fart (like me) would have to pay $900.

Of course many old farts hung on to their corporate jobs, or just went uninsured and prayed for the day they turned age 65. (when their total premium for Parts A and B (with a $150 Part B deductible) is about $110 a month.)

This incredible inequality between a 63 year old and a 65 year old is old hat to a private sector actuary. But why both political parties have tolerated this sometimes seems beyond belief to me.

The ACA chopped away at this grotesque unfairness for persons making less than about $40K a year, or $62K per couple. It was a good gesture, and Republican fat cats have been very slow to recognize this. In my reading, the persons who call for a return to full underwriting tend to have nice secure federal coverage for themselves. They are a bunch of limousine Darwinists, as Uwe Reinhardt has pointed out.

I think it is just inertia. It may be urban myth, but I was always taught that 65 became the retirement age when Bismarck instituted the first pension plan for Prussian civil servants.

He asked some question about the 75th percentile or 90th percentile (or something like that) for their life expectancy. The answer was 65, so that is the age he chose!