A Bill to Establish a Single-Payer Health System Advances in California

A bill has passed its first legislative hurdle to establish a government-run program of universal coverage in California. The California Senate Health Committee passed the measure 5-2. Next it will be debated by the Senate Appropriations Committee. The sticking point is how to fund such an endeavor.

A bill has passed its first legislative hurdle to establish a government-run program of universal coverage in California. The California Senate Health Committee passed the measure 5-2. Next it will be debated by the Senate Appropriations Committee. The sticking point is how to fund such an endeavor.

The bill, SB 562, would establish a publicly run healthcare plan that would cover everyone living in California, including those without legal immigration status. The proposal would drastically reduce the role of insurance companies: The state would pay for all medical expenses, including inpatient, outpatient, emergency services, dental, vision, mental health and nursing home care.

When the issue was studied in both Vermont and Colorado, backers were looking at higher income taxes and dedicated payroll taxes of about 10%. Yet both programs were going to run in the red from day one, with deficits getting larger throughout the following years.

People who support Single-Payer type Medicaid-for-All programs often do not really understand how they are supposed to work. Single-payer programs like Medicare are increasingly turning to private managed care providers to care for seniors. Even fee-for-service (FFS) Medicare is looking for ways to make the program into managed care through Accountable Care Organizations (ACOs).

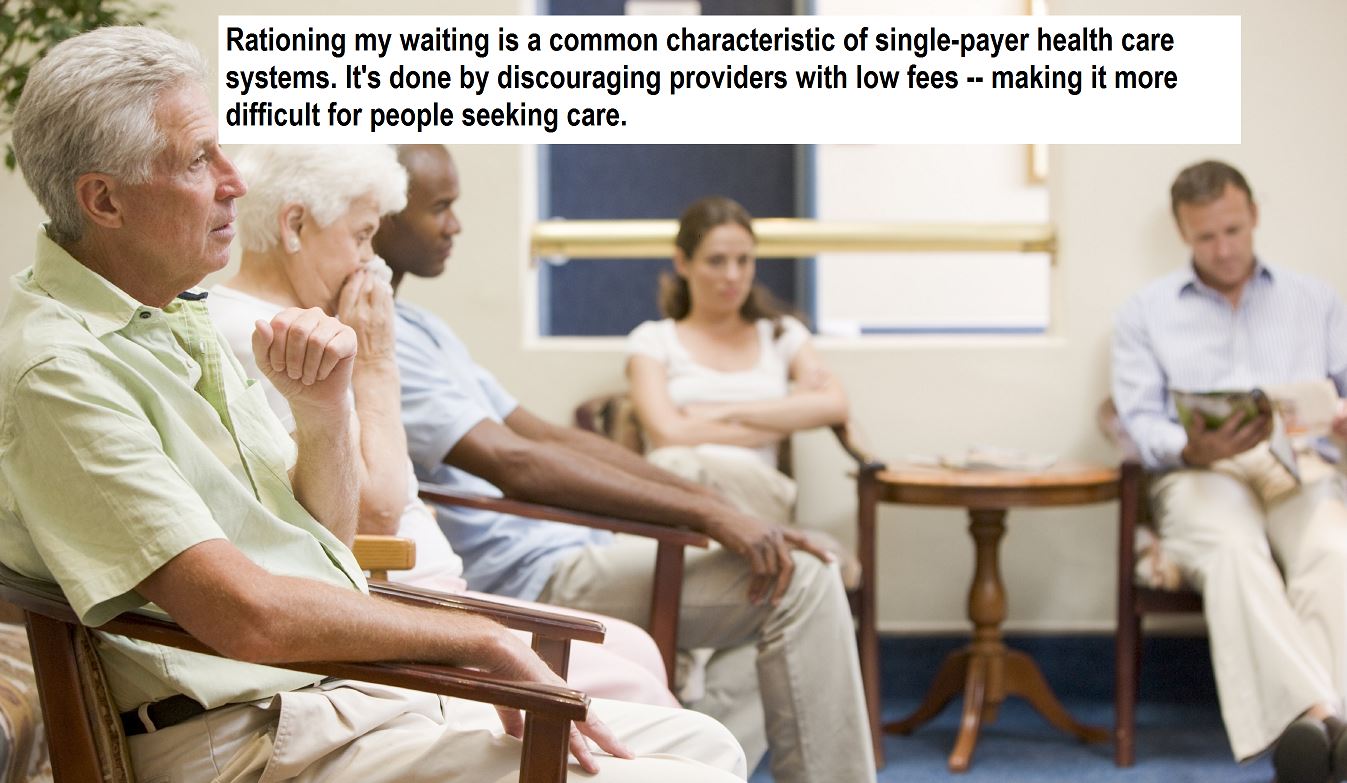

To be sustainable, a single-payer program in the United States would have to be run as the (nearly) sole payer for medical care. It would have to use monopsonistic powers to drive down provider fee to something below where the quantity supplied and quantity demanded curves intersect. For you non-economists, this means fees would be to be below the market clearing price resulting in mild shortages. That would result in what’s known as rationing by waiting. Such a system would have to aggressively combat fraud. A single-payer would have to scrutinize hospitals’ Medicare cost reports and pay global budgets with only small bundled payments for actual services. On average, the fees paid to providers would have to be lower than Medicare but probably above Medicaid reimbursements. Price controls are typically used to set prices for drugs and supplies, like is common in Canada, Britain, New Zealand, etc. Services are always rationed.

The error these shortsighted proposals suffer from is they want everyone to have Gold Plated health insurance. That is not how single payer programs work. A better idea rarely used in single payer systems would require consumers to pay for their own primary care out of pocket and have the governmental entity only provide catastrophic care. Only then would payroll taxes of 10% sustain such a program — and possibly that would not even be enough.

As you can see, Single-Payer Utopia is a pipe dream. Americans will never tolerate the overt rationing necessary to provide universal Medicaid-for-All program funded by other peoples’ money.

The California Constitution says they can’t print money so they are doomed. Poor Governor Brown. When Trump’s tax Reform hits and the home mortgage deduction is ELIMINATED the California property prices will drop like a rock creating a buying frenzy and those Valley Girls and Beach Boys will lose their Ocean Front Beach Property because they will have to sell dirt-cheap.

Can’t you just picture the future. All of those pesky deductions gone except those other taxed retirement accounts and America’s BEST tax dodge, the tax-free HSA, it’s beautiful.

Then we will advertise: HSAs are BIGGER, BETTER, BOLDER and BEAUTIFUL. America’s 1st HSA enrolled at Save101.com

Most policy analysts understand how the tax exclusion for employer-sponsored health insurance has promoted wasteful health plans that drives up medical costs. The tax exclusion for state income taxes (like California) also drives up state spending.

Devon, It is worse than anybody could imagine. The Sate of Kentucky is being raped by Anthem Blue Cross. Check out the stupidity of Rand Paul:

Ron Greiner wrote on April 29, 2017 07:21 AM :

Rand Paul is lost and says, “Those groupings would give smaller insurance customers “leverage of buying power through size,” Everybody knows that Individual Medical (IM) insurance is less expensive than Group insurance. For example: Kentucky State employees (Big Group) pays $1,595.48 a month for a 30-year-old couple to evil Anthem Blue Cross Inc. The Out-Of-Pocket is $2,750 per year, per person. That is a whopping $4,786.44 per quarter! In contrast, the Individual Medical (IM) insurance product called Short Term Medical (STM) is cheaper. This same couple, in Bowling Green zip code 42101, can get STM PPO with a SMALLER $2,500 deductible then 100% coverage for $467.25 per quarter which is less than 10% of the OVER-PRICED Group. BUT, the couple must pay an additional $15 a month because it is an ASSOCIATION health plan!

Adam Meier, Gov. Matt Bevin’s deputy chief of staff for policy, says to get association health plans and I quote, “you’re going to have to pass an ERISA-type (Employee Retirement Income Security Act) federal legislation that would preempt all the state laws,” Kentucky’s tax dollars are paying for stupid policy wonks because I sell association health plans NOW. It’s impossible to get good help these days.

Rand Paul has never paid taxes on his over-priced employer-based health insurance but poorer Kentucky women earning $49,000 get NO Obamacare tax credits on the Exchange and must purchase expensive GUARANTEED ISSUE Obamacare plans, HMOs that pay NOTHING if they go out-of-network, with sky-high Out-Of-Pockets (OOP) of $7,150 a year with AFTER-TAX-DOLLARS which makes it even more expensive.

Rand Paul thinks age-based tax credits so this poorer Kentucky woman can get some tax relief, like he has ALWAYS enjoyed, is an ENTITLEMENT like Obamacare that he can’t live with, what a selfish jerk.

I would never debate Rand Paul over eye surgery because he would win. BUT, because I enrolled the USA’s 1st tax-free HSA and I’m licensed to sell insurance coast to coast and I know all of the laws I would debate this selfish uninformed Kentucky jerk in a New York minute and he wouldn’t stand a chance. It would be like taking candy from a baby, a blind baby.

http://mycn2.com/politics/sen-paul-says-nobody-wants-war-against-north-korea-as-tensions-escalate#cpreview

Dental, vision, mental health and nursing home!

Excellent idea. I’m not sure doubling the state budget would even come close to covering the costs. I hope to god this passes so I can send MOM to a nursing home in California.

I love how they say in section 1 that the PPAC and ACA made great improvements to health care and then every paragraph after that states problems..

The people of the State of California do enact as follows:

SECTION 1. (a) The Legislature finds and declares all of the following:

(1) All residents of this state have the right to health care. While the federal Patient Protection and Affordable Care Act (PPACA) brought many improvements in health care and health care coverage, it still leaves many Californians without coverage or with inadequate coverage.

(2) Californians, as individuals, employers, and taxpayers taxpayers, have experienced a rise in the cost of health care and health care coverage in recent years, including rising premiums, deductibles, and copays, as well as restricted provider networks and high out-of-network charges.

(3) Businesses have also experienced increases in the costs of health care benefits for their employees, and many employers are shifting a larger share of the cost of coverage to their employees or dropping coverage entirely.

(4) Individuals often find that they are deprived of affordable care and choice because of decisions by health benefit plans guided by the plan’s economic needs rather than consumers’ health care needs.

(5) To address the fiscal crisis facing the health care system and the state, and to ensure Californians can exercise their right to health care, comprehensive health care coverage needs to be provided.

(6) It is the intent of the Legislature to establish a comprehensive universal single-payer health care coverage program and a health care cost control system for the benefit of all residents of the state.

(b) (1) It is further the intent of the Legislature to establish the Healthy California (HC) program to provide universal health coverage for every Californian based on his or her ability to pay and funded by broad-based revenue.

(2) It is the intent of the Legislature for the state to work to obtain waivers and other approvals relating to Medi-Cal, the state’s Children’s Health Insurance Program, Medicare, the PPACA, and any other federal programs so that any federal funds and other subsidies that would otherwise be paid to the State of California, Californians, and health care providers would be paid by the federal government to the State of California and deposited in the Healthy California Trust Fund.

(3) Under those waivers and approvals, those funds would be used for health coverage that provides health benefits equal to or exceeded by those programs as well as other program modifications, including elimination of cost sharing and insurance premiums.

(4) Those programs would be replaced and merged into the HC program, which will operate as a true single-payer program.

(5) If any necessary waivers or approvals are not obtained, it is the intent of the Legislature that the state use state plan amendments and seek waivers and approvals to maximize, and make as seamless as possible, the use of federally matched public health programs and federal health programs in the HC program.

(6) Thus, even if other programs such as Medi-Cal or Medicare may contribute to paying for care, it is the goal of this act that the coverage be delivered by the HC program, and, as much as possible, that the multiple sources of funding be pooled with other HC program funds and not be apparent to HC program members or participating providers.

(c) This act does not create any employment benefit, nor does it require, prohibit, or limit the providing of any employment benefit.

Its Free. Don’t let Nancy read it just please pass this!

CHAPTER 3. Eligibility and Enrollment

100620. (a) Every resident of the state shall be eligible and entitled to enroll as a member under the program.

(b) (1) A member shall not be required to pay any fee, payment, or other charge for enrolling in or being a member under the program.

(2) A member shall not be required to pay any premium, copayment, coinsurance, deductible, and any other form of cost sharing for all covered benefits.

(c) A college, university, or other institution of higher education in the state may purchase coverage under the program for a student, or a student’s dependent, who is not a resident of the state.

CHAPTER 4. Benefits

100630. (a) Covered health care benefits under the program include all medical care determined to be medically appropriate by the member’s health care provider.

(b) Covered health care benefits for members shall include, but are not limited to, all of the following:

(1) Licensed inpatient and licensed outpatient medical and health facility services.

(2) Inpatient and outpatient professional health care provider medical services.

(3) Diagnostic imaging, laboratory services, and other diagnostic and evaluative services.

(4) Medical equipment, appliances, and assistive technology, including prosthetics, eyeglasses, and hearing aids and the repair, technical support, and customization needed for individual use.

(5) Inpatient and outpatient rehabilitative care.

(6) Emergency care services.

(7) Emergency transportation.

(8) Necessary transportation for health care services for persons with disabilities or who may qualify as low income.

(9) Child and adult immunizations and preventive care.

(10) Health and wellness education.

(11) Hospice care.

(12) Care in a skilled nursing facility.

(13) Home health care, including health care provided in an assisted living facility.

(14) Mental health services.

(15) Substance abuse treatment.

(16) Dental care.

(17) Vision care.

(18) Prescription drugs.

(19) Pediatric care.

(20) Prenatal and postnatal care.

(21) Podiatric care.

(22) Chiropractic care.

(23) Acupuncture.

(24) Therapies that are shown by the National Institutes of Health, National Center for Complementary and Integrative Health to be safe and effective.

(25) Blood and blood products.

(26) Dialysis.

(27) Adult day care.

(28) Rehabilitative and habilitative services.

(29) Ancillary health care or social services previously covered by county integrated health and human services programs pursuant to Chapter 12.96 (commencing with Section 18986.60) and Chapter 12.991 (commencing with Section 18986.86) of Part 6 of Division 9 of the Welfare and Institutions Code.

(30) Ancillary health care or social services previously covered by a regional center for persons with developmental disabilities pursuant to Chapter 5 (commencing with Section 4620) of Division 4.5 of the Welfare and Institutions Code.

(31) Case management and care coordination.

(32) Language interpretation and translation for health care services, including sign language and Braille or other services needed for individuals with communication barriers.

(33) Health care and long-term supportive services currently covered under Medi-Cal or the state’s Children’s Health Insurance Program (CHIP). Program.

(34) Covered benefits for members shall also include all health care services required to be covered under any of the following provisions, without regard to whether the member would otherwise be eligible for or covered by the program or source referred to:

(A) The state’s Children’s Health Insurance Program (CHIP) (Title XXI of the Social Security Act (42 U.S.C. Sec. 1397aa et seq.)).

(B) Medi-Cal (Chapter 7 (commencing with Section 14000) of Part 3 of Division 9 of the Welfare and Institutions Code).

(C) The federal Medicare program pursuant to Title XVIII of the Social Security Act (42 U.S.C. Sec. 1395 et seq.).

(D) Health care service plans pursuant to the Knox-Keene Health Care Service Plan Act of 1975 (Chapter 2.2 (commencing with Section 1340) of Division 2 of the Health and Safety Code).

(E) Health insurers, as defined in Section 106 of the Insurance Code, pursuant to Part 2 (commencing with Section 10110) of Division 2 of the Insurance Code.

(F) Any additional health care services authorized to be added to the program’s benefits by the program.

(G) All essential health benefits mandated by the Affordable Care Act as of January 1, 2017.

Sounds like they want to kill COBRA the same as they killed HIPAA.

I wonder if living in California and taking the single-payer instead of Medicare will forever disqualify people from joining Medicare in another state (or subject them to the 10% per year penalty).

Presumably, they will add Massage Therapy for fibromyalgia and Hypnosis for tobacco addiction to make it complete.

.

In the meantime, I hope the California Legislature is aware that the last catastrophic earthquake involving the Cascadia subduction occurred on January 26, 1700. Historical analysis suggests a similar occurrence at the level of the 2011 Japanese event every 240 years, on average. A geologist at Oregon State University has determined that there is a 40% chance of a catastrophic earthquake involving the southern margin of the Cascadia subduction fault near Cape Mendocino in northern California WITHIN THE NEXT 50 YEARS.

.

Exactly Paul, would you want your multi-million dollar home in earthquake targeted Southern California or Tampa Bay with NO State Income Tax, NO earthquakes and NO Democratic Governor?

In Tampa Bay you can say we are the home of the 2018 Super Bowl Champions instead of those creeps who refuse to stand during the Anthem. Besides, our palm trees are just as beautiful.

For real estate investing the new west coast is Tampa Bay.

Paul, since you are providing information on catastrophic geological events causing earthquakes along with due dates I’ll add EMP. EMP is a nationwide potential catastrophic event that also happens at intervals and one we are due for. EMP can lead to devastation of the national electrical grid and if big enough could place us back in the stone age. A nuclear bomb is one way of causing EMP, but events on the sun that occur at intervals do the same. In the past such events have caused electrical problems, but at the time the electrical infrastructure was not develped enough to cause catastrophic harm.

Tampa has America’s best real estate investment GURU Peter Fortunato. Use other peoples’ money to get your beautiful multi-million dollar home. Peter is a libertarian and a capitalist. He believes that transactions which you can be proud of result from carefully conceived goals and plans followed by purposeful actions and scrupulous documentation.

Peter Fortunato is economical. For Webster’s economical means careful, efficient use of resources.

You can use your tax-free HSA balance to purchase Florida real estate. Peter says, “Knowledge is more valuable than money.”

Pete Fortunato Answers THE question!!!! (1 minute 34 seconds)

https://www.youtube.com/watch?v=TCP6LKYs8NA

California: Widespread Panic NCPA NEWSFLASH:

California’s insurance regulator will let insurers file two sets of rates for health insurance depending on what happens to Obamacare next year: regular Obamacare rates and “Trump rates.”

Insurers can file regular Affordable Care Act rates, which assume no major changes in the law.

But they can also file “Trump rates,” which would reflect the higher rates they would have to charge if Congress succeeds in repealing the law’s individual insurance mandate and if federal funding for cost-sharing reduction payments isn’t provided. The Trump administration has threatened to withhold those payments, which are meant to help companies offset the cost of lower premiums for low-income people.

Still, California’s decision to allow for two sets of rates is a nod to growing uncertainty among insurers about the Trump administration’s intentions, and whether Congress will get anywhere in repealing parts of the law.

Insurers have to file rates with California by next week, and the state’s insurance commissioner, [Dave Jones], criticized Republicans’ ongoing effort to repeal the law.

[Dave Jones] is Save101.com’s audio guy, the VOICE of the tax-free HSA. Here is a sample of Dave’s HSA VOICE: (1 minute)

https://www.youtube.com/watch?v=y18j6MXmr_E

National politics run amok!

Oregon Obamacare Nightmare

— Insurance companies selling 2018 policies in Oregon have [[two weeks]] to figure out how much they’ll charge, what they’ll sell and where. That’s no easy task, given the federal government could send it all tumbling down.

The uncertainty has already prompted Oregon insurance regulators to push back the deadline for companies to submit their proposed 2018 premiums, or monthly rates, from Monday to May 15. That sets off a monthslong process in which analysts in the state’s Department of Consumer and Business Services review and tweak proposed prices, hear companies’ rebuttals and make final decisions. Prices are scheduled to be finalized July 20.

But given the sheer number of things that could happen between now and then, the process is shaping up to be a [[wild ride]].

A side effect of having fewer choices in 2017 was the disappearance of policies, at least in Central Oregon, that let members put money into [[health savings accounts]] — tax-advantaged accounts that help people pay for out-of-pocket medical expenses their health insurance policy doesn’t cover.

That won’t be the case in 2018, Cutler said, as his office [[will ensure]] all standard bronze policies, a type of policy marketplace carriers are required to offer, will let people use their HSA accounts.

“[[It’s a lesson learned]], I think,” he said of the lack of HSA-compatible policies available this year.

Perhaps the biggest lingering question mark for insurance companies is whether the Trump administration will continue to fund billions of dollars the federal government has provided each year to insurers under the Affordable Care Act. So-called cost-sharing reduction payments — which amounted to an estimated $7 billion in 2016 — reimburse insurers for reducing out-of-pocket costs for low-income members. They’re separate from the Affordable Care Act’s tax credits that help people afford their premiums.

Those payments are the subject of a lawsuit from the U.S. House of Representatives that takes issue with how they’re funded. The Obama administration had defended the payments. It’s unclear whether the Trump administration will do the same.

If those payments go away, insurers will have to [[eat the losses]], stop selling marketplace policies or raise their prices. Molina Healthcare, which doesn’t sell policies in Oregon, has said it will [[leave the marketplace]] if the cost-sharing reduction payments aren’t funded.

The Trump administration probably won’t stop those payments in 2017, a move that would cause “absolute chaos,” but 2018 is still unclear, said Jeff Luck, associate professor of health management and policy at Oregon State University.–

— Reporter: 541-383-0304

It is a brave new world when Oregon Regulators DEMAND that insurance companies offer consumers tax-free HSA Qualifying insurance. The NCPA really started something.

When the CA legislature gets around to trying to figure out how to pay for their single payer health insurance plan, it will find that the force of idealism is lost when it fails to recognize the reality of things. Don’t even get me started on issues ranging from the potential for fraud to patients wanting to see their doctor for every sniffle just to seek reassurance since no cash is due at the point of service. Doctors may also find that patients will suddenly think nothing of just not showing up for appointments and not calling to cancel again because no cash is due at the point of service. This has long been an issue in Canada, especially for primary care doctors.

Barry, those Beach Boys and Valley Girls think that Medicaid and SCHIP will be block grants but Medicaid payments are going down and SCHIP is up for re-authorization this year and we should terminate the program because it is too dangerous for children.

President Trump’s age-based tax credits are meant for the purchase of personal, portable and permanent Individual Medical (IM) insurance and California’s single payer sounds like ONE big group to me so NO tax credits for California.

It looks like even California’s current funding is going to dry up. Please, the last person to leave California, turn off the lights.

It makes me wonder if single-payer initiatives like California’s aren’t just a feel-good gestures Maybe they’re hoping to nudge the US federal government in that direction since CA has to balance its budget and the federal government can just borrow against future generations of taxpayers.

Even liberal CA governor, Jerry Brown, is skeptical about how CA would ever be able to pay for its single payer system as proposed. From the description above, it sounds like it could easily cost $300 billion per year if not more to cover CA’s population of 40 million with no cash at the time of service from patients and full coverage of long term custodial care.

My question isn’t where’s the beef; it’s where’s the financing plan. Talk is cheap. Money is where the rubber meets the road.

Even for the feds, replacing ESI and IM with taxpayer funded coverage, reducing patient contributions toward their care and extending coverage to long term custodial care would be a mighty heavy lift. It would probably take a VAT with a 15% rate, which would raise revenue equal to 6% of GDP, to even attempt this at the federal level and that assumes both Medicare and Medicaid along with VA care stay in place.